Abstract

This paper will focus on several aspects of trading, and how it has been revolutionised as a result of the advancements of financial technology. The first section introduces the reader to the history of trading by explaining its origins and describing its gradual progression up until the present. The following section analyses what is perhaps the most advanced and modern element of trading – cryptocurrencies. The two sections not only provide the reader with knowledge on what cryptocurrencies consist of, but also contain the different methods and websites used for trading cryptocurrencies. Naturally, our study also looks at the use of trading within banks, laying out in detail how the use of trading strategies and algorithms continues to modernise the industry. Additionally, this paper also examines trading for individuals, and how anyone can use financial technology to their advantage. This section assesses different trading strategies, using the example of Forex trading, while also evaluating the benefits and shortcomings of financial technology. Finally, the main body of the paper is concluded by theories on what the future beholds for both trading and financial technology, assessing several possible advancements.

Introduction

The concept of financial technology was first introduced back in 1967, in the Boston Globe newspaper. The world of finance has never been the same since, as the introduction of technology destined it for an eternity of constant change. Even now, where the use of technology and programming in finance seems to be functioning effectively, there are still continued attempts to expand the potential capacity of fintech. Now with every financial institution annually investing billions into technological software, it is only natural that trading has evolved immensely since the formation of the first stock exchange in Amsterdam in the 17th century – and even since the early days of Wall Street. With new technologies making trading more accessible to the public, now any individual has the invitation to the world of endless possibilities, as trading platforms are only ever a few clicks away. Yet, financial technology has not only increased the popularity and accessibility of trading, it has also revolutionised the functionality. The creation of algorithmic trading and high-frequency trading have had a significant impact on both the speed and scale of operations. In this paper, we will aim to analyse how technological progress has reformed the trade industry, through the examples of cryptocurrency, banks, and everyday trading for individuals, before theorising about future developments.

History of Trading

Trading has always been present in human life, first dating back to 320,000 years ago with the early humans located in East Africa who began trading manufactured goods and colour pigments with distant groups. For thousands of years, trade has been a vital component of the global economy, but as societies became increasingly complex over time, the demand for a more efficient means of exchange arose; as a result, currency was created and developed. Trade networks expanded along with communities. Global trade was sparked by the Age of Exploration in the 15th and 16th centuries, which resulted in the creation of colonial marketplaces and the exchange of goods like tobacco, sugar, and spices. During this time, mercantilism also began to take shape as countries looked to expand their colonies and create surpluses in order to increase their wealth. Centuries later, countries began to industrialise. Trade procedures were drastically changed throughout the Industrial Revolution in the 18th and 19th centuries. Transportation was revolutionised with the advent of steam-powered ships and railways, which made it possible for products to be transported over long distances more quickly. There was no overarching theory of trade and industrial policy at the time, since each country had unique circumstances and needed unique policies at any particular period. For example, during the 19th century, the United States saw rapid expansion due to its protectionist policies. During the 1829–1831 to 1909–1911 period, the United States is estimated to have grown at an average annual rate of 2.4, compared to 1.2 for Western Europe. Specifically, the country was able to quickly overtake Great Britain in terms of GDP per capita, technological advancement, and export performance, thanks to the escalation of protectionism after 1860.

Stock exchanges were also established during this time, with the Amsterdam Stock Exchange emerging as the first recognised stock market in history early in the 17th century. Innovations in technology continued to change the face of trading later in the 20th century. Decisions about market trading could be communicated more quickly with the introduction of the telephone and telegraph, which resulted in more informed decisions. A significant advance forward was made possible by the development of computerised trading systems in the latter half of the 20th century, which made trading more accurate and efficient. The 21st century saw the New York Stock Exchange make the switch to electronic trading, which marked a significant change in the way that trades could be conducted.

The evolution of trading has been further encouraged by recent technological advancements. Retail investors can now trade from home thanks to the democratisation of financial markets brought about by the growth of the internet. People can now buy and sell assets, trade currencies and cryptocurrencies, and participate in the stock market with greater ease thanks to online trading platforms and mobile applications.

With the launch of Bitcoin in the late 2000s, cryptocurrencies emerged and changed the trade market. Blockchain technology powers these decentralised digital currencies, allowing for peer-to-peer transactions devoid of mediators. A new asset class has emerged as a result of the expansion of cryptocurrency exchanges, drawing interest from institutional and ordinary investors.

Technological developments and societal shifts have affected every stage of development. In an increasingly interconnected global economy, the integration of developing technologies will continue to change the trading landscape as time goes on, posing both new opportunities and complications for traders.

Cryptocurrency: What Is It?

Cryptocurrency, often referred to as crypto, is a form of digital or virtual currency that utilises cryptography for security, making it nearly impossible to counterfeit or double-spend. Unlike traditional currencies issued by governments, cryptocurrencies operate on decentralised networks based on blockchain technology – a distributed ledger enforced by a network of computers (nodes). The most well-known cryptocurrency, Bitcoin, was introduced in 2009 by an anonymous entity known as Satoshi Nakamoto and has since paved the way for thousands of other cryptocurrencies, including Ethereum, which introduced the concept of smart contracts (Tapscott & Tapscott, 2016). These smart contracts are self-executing agreements where the terms are directly written into code, allowing for automated and transparent transactions without the need for intermediaries. The blockchain technology underlying cryptocurrencies ensures that all transactions are recorded in a secure and immutable manner, thus fostering trust and reducing the need for centralised authority (Nakamoto, 2008). Crypto transactions are facilitated through digital wallets, which store the public and private keys required to access and transfer funds, and are typically managed through various exchanges where users can trade cryptocurrencies for other assets or fiat currencies (Narayanan et al., 2016). Cryptocurrencies offer several advantages over traditional financial systems, including lower transaction fees, faster processing times, and increased financial inclusion, particularly for individuals in underserved regions. However, they also face significant challenges, such as regulatory scrutiny, market volatility, and concerns over illicit activities due to their pseudonymous nature (Catalini & Gans, 2016). The regulatory environment for cryptocurrencies is evolving, with governments around the world working to develop frameworks to address these concerns while balancing innovation with consumer protection. Despite these challenges, the growing adoption of cryptocurrencies and blockchain technology in various sectors, from finance to supply chain management, indicates their potential to transform multiple aspects of the global economy

The Role of Cryptocurrencies in Trading

Cryptocurrency sites have become essential hubs for individuals and institutions engaging in the burgeoning world of digital finance, where the rapid rise of blockchain technology has introduced numerous currencies, each with unique attributes and purposes. These platforms, ranging from exchanges like Binance, Coinbase, Kraken, and decentralised platforms such as Uniswap and PancakeSwap, serve as gateways for trading, buying, selling, and managing digital currencies. The cryptocurrency ecosystem is vast and complex, with thousands of different digital currencies, also known as altcoins, each contributing to the evolving landscape of decentralised finance (DeFi).

Bitcoin (BTC), the pioneer cryptocurrency, remains the most well-known and widely accepted digital currency, often referred to as digital gold for its store of value. However, the ecosystem has expanded significantly beyond Bitcoin to include various other major cryptocurrencies like Ethereum (ETH), which is widely regarded for its smart contract capabilities that power decentralised applications (dApps), non-fungible tokens (NFTs), and various DeFi protocols. Ethereum’s blockchain technology has paved the way for innovation, allowing developers to build decentralised applications across multiple industries, from finance to gaming, creating a vibrant community around its currency, Ether. Litecoin (LTC), a peer-to-peer cryptocurrency, was created as a lighter and faster version of Bitcoin, with quicker transaction times and lower fees, making it suitable for smaller transactions and daily purchases. Ripple (XRP) is another prominent cryptocurrency, specifically designed for facilitating fast, low-cost international payments, particularly between financial institutions, aiming to disrupt the traditional SWIFT system used in global banking. The rise of stablecoins like Tether (USDT), USD Coin (USDC), and Binance USD (BUSD) has also added a layer of stability to the often volatile cryptocurrency market. These stablecoins are pegged to traditional fiat currencies, primarily the U.S. dollar, providing traders with a reliable means of transferring value without being subject to the drastic price swings commonly associated with other cryptocurrencies. The advent of DeFi has seen the proliferation of various decentralised currencies like Chainlink (LINK), which focuses on providing decentralised oracle networks to connect smart contracts with real-world data, and Aave (AAVE), a decentralised lending protocol that allows users to lend and borrow cryptocurrencies without the need for intermediaries. As the cryptocurrency market continues to evolve, new and innovative projects are continually emerging, such as Polkadot (DOT), which aims to enable cross-blockchain transfers of any type of data or asset, and Solana (SOL), which is praised for its high throughput and low transaction costs, positioning itself as a competitor to Ethereum in the dApp and DeFi space.

The proliferation of these digital assets has not only expanded the financial opportunities available to individuals, but has also raised numerous regulatory and security concerns. Cryptocurrency exchanges and wallets must adhere to stringent security protocols to protect users’ funds from hacking and fraud, and many platforms have implemented two-factor authentication (2FA), cold storage, and insurance policies as part of their security measures. Despite these efforts, the decentralised nature of cryptocurrencies means that users must remain vigilant and take responsibility for their security, as transactions on most blockchain networks are irreversible and can result in permanent loss of funds if mishandled. The regulatory landscape surrounding cryptocurrencies varies widely across different countries, with some governments embracing the technology and others implementing strict regulations or outright bans. In the United States, for example, the Securities and Exchange Commission (SEC) and the Commodity Futures Trading Commission (CFTC) have taken an active role in regulating the market, particularly concerning initial coin offerings (ICOs) and cryptocurrency derivatives, to ensure investor protection and market integrity. On the other hand, countries like El Salvador have taken a more progressive stance, with El Salvador becoming the first country in the world to adopt Bitcoin as legal tender in 2021, a move that has sparked both praise and criticism from the international community.

The rapid development of central bank digital currencies (CBDCs) is also shaping the future of money, with countries like China leading the way with the digital yuan, which is currently being tested in various cities across the country. CBDCs are digital versions of fiat currencies issued and controlled by central banks, offering the potential for more efficient and secure transactions while providing governments with greater control over monetary policy and financial systems. While CBDCs and decentralised cryptocurrencies share some similarities in their digital nature, they differ significantly in terms of their underlying principles, with CBDCs being centralised and controlled by governments, whereas cryptocurrencies like Bitcoin are decentralised and operate on peer-to-peer networks without a central authority.

The rise of non-fungible tokens (NFTs) has also captured the attention of the cryptocurrency world, with NFTs representing unique digital assets such as artwork, music, videos, and in-game items that can be bought, sold, and traded on blockchain networks like Ethereum. NFTs have revolutionised the way digital content is owned and monetised, giving creators new opportunities to engage with their audiences and generate revenue. However, the NFT space is not without controversy, as concerns about environmental impact, copyright infringement, and speculative bubbles have led to ongoing debates within the crypto community.

The cryptocurrency ecosystem continues to expand and evolve, with new innovations and challenges emerging regularly, making it an exciting yet complex space for investors, developers, and enthusiasts alike. Crypto sites play a critical role in this ecosystem, providing the necessary infrastructure for accessing, trading, and managing digital assets, while also serving as educational resources for those looking to learn more about the technology and its potential applications. Whether through centralised exchanges, decentralised finance platforms, or blockchain-based applications, the cryptocurrency space offers a diverse range of opportunities for individuals to participate in the future of finance, while also presenting new challenges in terms of security, regulation, and sustainability.

Trading Within Banks

One of the most significant changes in bank trading is the adoption of automation and AI. In years past, human traders made decisions based on market analysis, intuition, and experience. However, the creation of AI and machine learning algorithms have revolutionised this process by enabling the automation of trading decisions. AI algorithms can process huge amounts of data, identify patterns, and execute trades much faster than humans ever could.

These algorithms use complex models to make decisions about buying and selling securities at the optimal times. They can analyse market trends, historical data, and even news events to predict price movements. For banks, this means greater efficiency, reduced human error, and the ability to capitalise on market opportunities more effectively.

AI-driven trading systems have also made it possible for banks to engage in high-frequency trading (HFT), where large volumes of transactions can be executed within fractions of a second. This type of trading relies on speed and precision, areas where AI is much more effective than humans. However, while HFT can lead to significant profits, it also raises concerns about market stability and fairness, as these systems can sometimes cause extreme volatility.

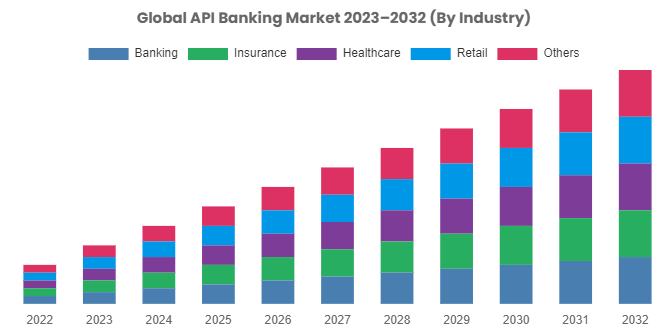

Digital platforms and Application Programming Interfaces (APIs) have become crucial to banks in the fintech era. These technologies allow banks to integrate their systems with fintech solutions, creating a more seamless and efficient trading environment. APIs enable different software systems to communicate with each other, allowing banks to offer real-time data, execute trades, and provide personalised services to clients.

For example, trading platforms now offer sophisticated tools that were once exclusive to large financial institutions. These tools include advanced risk management features, real-time analytics, and automated trading capabilities. By leveraging these digital platforms, banks can enhance their service offerings, improve customer experience, and remain competitive in an increasingly digital world.

Moreover, the integration of APIs with fintech applications allows banks to offer more customised products and services. Clients can access a range of financial products through a single platform, from traditional banking services to trading and investment options. This not only improves customer satisfaction but also enables banks to tap into new revenue streams.

Another significant development in the banking sector is the rise of digital-only banks, also known as neobanks. These banks operate entirely online, without physical branches, and leverage fintech to offer a wide range of financial services, including trading. The emergence of neobanks has introduced new competition for traditional banks, particularly in attracting tech-savvy customers who prefer the convenience of digital services.

Neobanks typically offer lower fees, more user-friendly interfaces, and innovative products compared to traditional banks. This has made them particularly appealing to younger generations and individuals who are comfortable managing their finances online. As a result, traditional banks have been forced to enhance their digital offerings to keep pace with these new entrants.

The success of neobanks has also led to increased investment in fintech, with many traditional banks forming partnerships with fintech companies to improve their digital capabilities. By collaborating with fintech firms, banks can offer more innovative trading solutions, such as robo-advisors, which provide automated, algorithm-driven financial planning services with minimal human intervention.

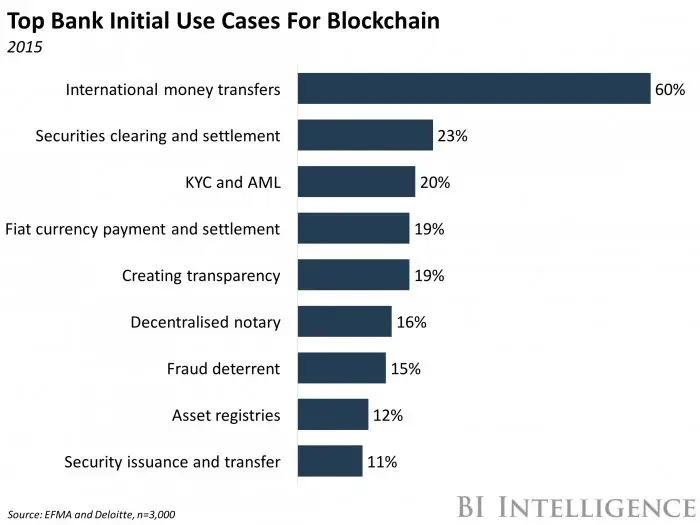

Blockchain technology and Decentralised Finance (DeFi) are other huge innovations in the banking industry, particularly in the context of trading and personal finance. Blockchain is the technology behind cryptocurrencies like Bitcoin and Ethereum. These cryptocurrencies rely on the blockchain as a decentralised ledger that records transactions across a network of individual computers. The main difference is that there is no large bank or government institution that controls these transactions, which essentially means that all transactions are anonymous. This technology offers several advantages for trading, including reduced transaction costs, and enhanced security.

In the traditional financial system, transactions require third parties such as banks or clearinghouses, which can add additional fees and occasionally delays. Blockchain eliminates the need for these intermediaries by allowing peer-to-peer transactions to occur directly between parties. This not only speeds up the transaction process but also secures the ledger as it is both decentralised and impossible to edit.

Decentralised Finance takes the principles of blockchain a step further by creating financial tools that are universally available. DeFi platforms offer services that are similar to traditional banks, like lending, borrowing, and trading, without the need for a central authority. For banks, this presents both a challenge and an opportunity. While DeFi has the potential to disrupt traditional financial services, it also offers new ways for banks to innovate and expand their offerings.

As banks increasingly adopt fintech solutions, they face new regulatory challenges. The integration of AI, digital platforms, and blockchain into trading operations requires banks to navigate complex regulatory landscapes. Ensuring compliance with evolving regulations, particularly concerning data privacy and cybersecurity, is crucial for maintaining customer trust and avoiding legal penalties.

The rise in digital transactions has also heightened the risk of cyber threats. As banks move more of their operations online, they become more vulnerable to cyberattacks, which can lead to significant financial and reputational damage. To mitigate these risks, banks must invest in robust cybersecurity measures, including encryption, multi-factor authentication, and continuous monitoring of their systems.

Moreover, the regulatory environment is still catching up with the rapid pace of fintech innovation. Regulators around the world are grappling with how to oversee new financial technologies while encouraging innovation. This balancing act is particularly challenging in areas like AI-driven trading and DeFi, where traditional regulatory frameworks may not be sufficient to address the unique risks posed by these technologies.

Effects of Financial Technology on Everyday Trading

With the preceding section introducing the concept of algorithmic trading, which involves the use of AI technology to raise the efficiency and speed of trades, we can now consider how traders can make use of financial technology.

In order to illustrate the effects of algorithmic trading on everyday operations, we shall focus on the example of Forex trading, which is now completely dominated by technology with 92% of trades in the Forex market in 2019 being performed by trading algorithms. Forex trading, or foreign exchange trading, consists of the purchase of one currency and the sale of another, in an attempt to profit from the transaction. The aforementioned Forex market is, in turn, the platform on which these currency operations occur. However, as the platform is open 24 hours a day, five days a week, it becomes nearly impossible for humans to track the highly dynamic price changes, and thus the most profitable purchase and sale price is difficult to attain. Hence, the use of algorithmic trading has gained immense popularity amongst Forex traders, due to its ability to conduct the trades automatically, quicker than with manual trading. In the case of Forex trading, different types of algorithms can be created. More simple ones, which essentially considers only the entry and exit point, as well as more complex varieties, which also take into account historical trades and live news.

Apart from the speed of transactions, algorithmic trading also offers the advantage of scale. Whereas a human is capable of focusing on one transaction and one trading strategy at a time, hundreds of algorithms can be programmed to run at the same time, operating with different currencies and different strategies. The ability to use different trading strategies simultaneously is a particularly groundbreaking advantage of algorithmic trading, as different tactics have their own benefits, and thus by using many of them, profit can be maximised.

One of the most popular trading strategies is scalping. This involves holding on to currencies for a very short period of time, sometimes a couple seconds, and selling them for a small profit following a price change. As price changes occur constantly on the Forex market, this may be a highly profitable strategy, if enough trades are made. This is exactly why traders turn to their algorithms, as hundreds of trades can be made throughout the day, and the small profit earned from each individual trade eventually builds up to a significant figure.

Another short-term strategy is day trading, where positions are held onto for a period of minutes or hours, and these are also often completed by algorithms as price changes are still too quick for the trader to monitor. However most other strategies, like swing or position trades, are long-term, meaning a trader can monitor the transaction manually, and hold on to the currency for days, months, or even years. Although algorithms can still be useful when operating using long-term strategies, as the computer can scan the market and analyse trends, the usefulness of the program decreases as the hold time of the currency rises.

However, while acknowledging the undeniable benefits for traders which arise from algorithmic trading, it is also important to assess the potential negatives. One of these is the potential of glitches and program malfunctioning. If there is a mistake in the programming, or an external issue, which disrupts the functionality of the algorithm, this will have significant consequences for the trader, especially if the scale of the operation is particularly great. For example, the algorithm glitching can lead it to buy the incorrect position, or the incorrect amount, meaning that the trader’s plan and strategy is not followed and this, potentially, will lead to monetary losses. If multiple algorithms malfunction at the same time, the financial hit on the trader will be even more damaging.

Another common misconception over algorithmic trading is that it is simple as the process is automated. If we stick with the example of Forex trading, the trader may be used to using the same set of strategies all of the time. Yet, as the market adapts and evolves at great speeds, the algorithm will also need to be altered to match. Thus, although the process of purchasing and selling market positions is indeed automated, the trader is still required to work on the programming of the algorithm in order to stay competitive within the market.

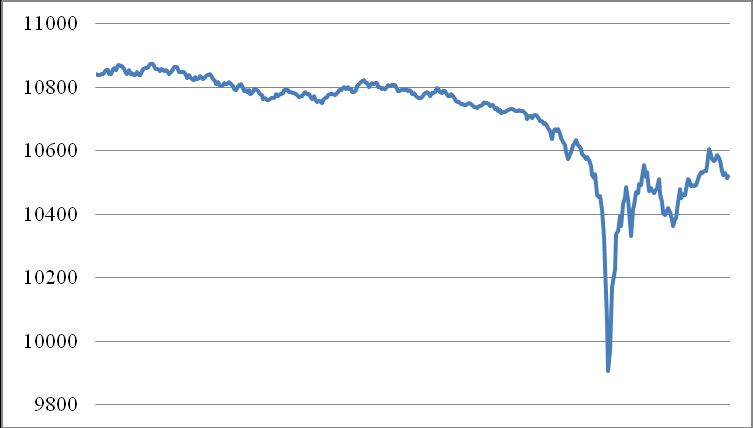

Additionally, besides the concerns regarding individual traders, there are also potentially global issues caused by the use of algorithmic trading. Due to the way in which most of the bots are programmed to operate, a small price decrease in a stock may trigger all of the algorithms to sell it off, resulting in a total collapse of its value. This phenomenon is referred to as a “flash crash”, as although stocks can suffer significant price drops in a short period of time, they regain most of their value in a matter of hours, sometimes even minutes. The most well-known example of a flash crash occurred on May 6th 2010, when the Dow Jones Industrial Average (DIJA) lost 9% of its total value within an hour, leading to the loss of over $1 trillion USD in equity. Although such an event is certainly rare and extreme, flash crashes still take place in the stock market. As outlined by the research of two mathematicians at the University of Michigan, the stock market experiences twelve flash crashes daily. In this way, such flash crashes have caused outrage across the world, and have led to serious discussions over the regulation, and even potential bans, of algorithmic trading. The most recent of such requests took place in China, in July of 2024, where several quantitative hedge funds faced heavy backlash for their use of financial technology.

Dow Jones, Flash Crash.

Overall, as demonstrated by the example of Forex trading, algorithmic trading provides an enticing opportunity for traders to increase the scale and speed of their operations. The automation of trades allows firms and individuals to attain the most profitable market positions when selling or purchasing. Nevertheless, algorithmic trading requires a cautiously prepared, complex program and constant surveillance to ensure that it operates adequately.

Future of Trading

The integration and advancements of financial technology have dramatically reshaped our methods of trading, resorting to methods such as cryptocurrency and artificial intelligence. In the next 50 years, the further development of financial technology will continue affecting trading, leading to a more efficient and interconnected global marketplace. The utilisation of artificial intelligence such as Machine Learning (ML), Deep Learning (DL), and Reinforcement Learning (RL) have demonstrated encouraging outcomes for boosting the general outcomes in market analysis, stock trading, and risk management, as well as decision-making processes and strategy optimisation. With AI, individuals are able to detect patterns in intricate economic data, which improves forecasts and predictions of future economic performance. Additionally, it can automate financial transaction processes, increasing efficiency, guiding decision making and optimising the accuracy of economic models. AI also has the potential to identify complex economic shifts and possible investment opportunities, making it an advantageous tool for people and companies. Currently, experienced traders are working towards integrating machine learning to accurately predict future stock values, although all products have unique characteristics, including market size and liquidity. Moreover, some investors are reluctant to rely on AI when it comes to trading due to its uncertainty. Therefore, the primary objective is to attempt merging multiple algorithms in order to increase the investor trust while lowering the potential risks. To ensure that AI becomes more reliable and continues to progress, tech companies are working towards the collaboration of two algorithms: Long Short-Term Memory (LSTM) and Auto-Regressive Integrated Moving Average (ARIMA). The combination of these two algorithms has the potential to create a more dependable and accurate model for investors to utilise.

As for cryptocurrency, it has already begun impacting the trading world. Researchers that look at the underlying blockchain, the legal ramifications of cryptocurrencies, and the technology’s economic and financial components have also become interested in cryptocurrency, as well as investors. Back in 2015, there were two primary factors which affected the growth of cryptocurrencies and their incorporation into the larger financial system: international government regulatory attempts, and conflicting public perception in moving towards its wider adoption. At the time and even at this moment, virtual currencies are not regarded as official means of paying, and in most countries are recognised as digital assets, a property rather than a currency. The currencies’ legal status needs to be established in order for them to become sustainable. Additionally, back in 2015 people were still largely unaware of cryptocurrency and how it functions. That same year, a survey done in April showed that only 4.5% of participants had ever used Bitcoin, the most prominent of the cryptocurrencies during that period of time. Over the next 50 years, a number of significant trends and advancements are expected to influence the direction of cryptocurrency. First of all, the widespread adoption of cryptocurrencies may eventually become the standard. Governments are likely to pass unified legislation to control the use of cryptocurrency, and regulatory frameworks are expected to become more clearly defined globally. A growing number of people might decide to use digital currencies for everyday transactions as they become more reliable and legitimate. This could result in a diverse environment where different cryptocurrencies have distinct functions. The emergence of central bank digital currencies, or CBDCs, might also drastically change the situation. The introduction of CBDCs could encourage greater acceptance of digital currencies globally, while also posing competition to currently-existing cryptocurrencies. Numerous countries are investigating or testing their own digital currencies, which may coexist with decentralised cryptocurrencies.

Blockchain technology is another fintech that has an impact on trading, its a dispersed database that keeps an ever-expanding collection of records in order called blocks. At the most basic level, they allow a group of users to record transactions in a shared ledger inside that group, so that once a transaction is published, it cannot be modified via standard blockchain network operations. Blockchain network users employ software to submit candidate transactions to the blockchain network. These transactions are sent by the software to a node or nodes in the blockchain network. Both publishing and non-publishing complete nodes may be among the selected nodes. The submitted transactions are subsequently distributed to the network’s other nodes, but this does not automatically add the transaction to the blockchain. A pending transaction in many blockchain implementations must wait in a queue until it is added to the blockchain by a publishing node after it has been distributed among nodes. A published block’s other full nodes will verify the legitimacy and validity of each transaction in it, and they won’t accept a block containing any invalid transactions. Blockchain may accelerate trade by eliminating the need for mediators and boosting party confidence by offering a safe, transparent, and permanent ledger. It’s possible that in 50 years there will be a completely decentralised market where parties can trade assets directly with one another without using conventional exchanges. Trade execution and settlement might be managed by smart contracts, which would further minimise expenses and boost productivity.

Conclusion

Ultimately, the development of financial technology has had a staggering impact on trading. With every trade now being conducted online, it is impossible to not acknowledge the pivotal role financial technology has played in the advancement of trading. Cryptocurrencies, especially, rely on modern technology, as they are a completely digital asset stored in an online wallet. Unlike other trading avenues, like stocks, cryptocurrencies did not exist at all prior to the development of sufficiently advanced financial technology, and the creation of the internet as a whole. Yet, despite the fact that other trading methods were available before the technological era, they have never been as efficient as now. Thus, banks have adopted AI and automated trading algorithms to facilitate new trading methods. The developed algorithms have many uses, the most notable of which is the capability to conduct high frequency trading, HFT, which massively reduces human error and boosts productivity. Perhaps, one of the greatest achievements of financial technology, in terms of trading, is the fact that it has massively boosted the availability of trading. Now, trading is not reserved only for brokers on Wall Street, which means the trade markets have many more active individual users, adding to the complexity of the industry. When it comes to algorithm trading, it has also become popular amongst individual traders, with 92% of trades on the Forex market being made by algorithm bots. Nevertheless, it is important to note that there are some downsides to financial technology in trading. These include the danger of information leakage, resulting in your personal information being stolen; the risk of a programming mistake, resulting in the algorithm bot making incorrect purchases; and also a global concern of algorithm trading, resulting in crashes of the market, as such was the case for the Dow Jones crash. However, all these can be prevented with the cautious storage of information and regulations, making them almost insignificant in comparison to the rewards arising from financial technology in trading. Thus, overall, financial technology has had an incredibly positive effect on trading, and will continue to revolutionise the industry for the foreseeable future.

Bibliography

A. M. Rahmani, B. Rezazadeh, M. Haghparast, W. -C. Chang and S. G. Ting. (2023). Applications of Artificial Intelligence in the Economy, Including Applications in Stock Trading, Market Analysis, and Ri. IEEE Access. 11(1), pp.80769-80793.

Alex Clere. (2022). How Digitisation has Transformed the Forex Market. [Online]. Fintech Magazine. Last Updated: 29 April. Available at: https://fintechmagazine.com/financial-services-finserv/how-digitisation-has-transformed-the-forex-market.

Alexander Keller and Michael Scholz. (2019). Trading on Cryptocurrency Markets: Analyzing the Behavior of Bitcoin Investors. [Online]. CORE. Available at: https://core.ac.uk/download/pdf/301384302.pdf.

Christian Catalini and Joshua S. Gans. (2016). Some Simple Economics of the Blockchain. [Online]. National Bureau of Economic Research. Available at: https://www.nber.org/papers/w22952.

Dylan Yaga, Peter Mell, Nik Roby and Karen Scarfone. (2018). Blockchain Technology Overview. [Online]. Arxiv. Available at: https://arxiv.org/pdf/1906.11078.

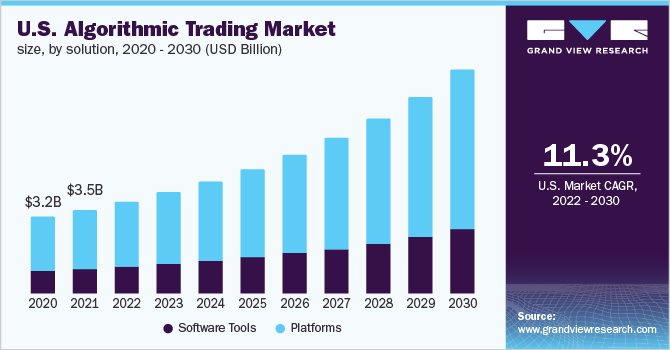

Georgia Weston. (2024). Algorithmic Trading in Fintech: A Game-Changer in Modern Finance. [Online]. 101 Blockchains. Available at: https://101blockchains.com/fintech-algorithmic-trading/.

Horizon Databook. (2021). Algorithmic Trading Market Size, Share & Trends Analysis Report By Solution, By Service, By Deployment, By Trading Types. [Online]. Grand View Research. Available at: https://www.grandviewresearch.com/industry-analysis/algorithmic-trading-market-report.

Insider Intelligence. (2017). Here’s How Banks Can Save Big With Blockchain. [Online]. Business Insider. Available at: https://www.businessinsider.com/heres-how-banks-can-save-big-with-blockchain-2017-1.

James Chen. (2024). How to Start Forex Trading: A Beginner’s Guide. [Online]. Investopedia. Last Updated: 29 August. Available at: https://www.investopedia.com/articles/forex/11/why-trade-forex.asp.

Lea Lobanov. (2023). Algorithmic Trading in Fintech: Leveraging Machine Learning and High-Frequency Trading. [Online]. Medium. Available at: https://medium.com/@lea.lobanov/

Mehdi Shafaeddin. (1998). How did Developed Countries Industrialise? The History of Trade and Industrial Policy: The Cases of Great Britain and th. UNCTAD. 139(1).

Michal Maliarov. (2024). How APIs Are Transforming Digital Banking in 2024. [Online]. Tapix. Available at: https://www.tapix.io/resources/post/how-apis-are-transforming-digital-banking-in-2024.

Mubasher Capital. (2024). What the is Fintech Trading?. [Online]. Mubasher Capital. Available at: https://mubashercapital.com/what-the-is-fintech-trading/#:~:text=Fintech%20trading%20platforms%20lev.

Ryan Farell. (2015). An Analysis of the Cryptocurrency Industry. [Online]. Core. Available at: https://core.ac.uk/reader/76387450.

Satoshi Nakamoto. (N/A). Bitcoin: A Peer-to-Peer Electronic Cash System. [Online]. www.bitcoin.org. Available at: https://bitcoin.org/bitcoin.pdf.

Troy Segal. (2024). The Ins and Outs of Forex Scalping. [Online]. Investopedia. Last Updated: 31 August. Available at: https://www.investopedia.com/articles/forex/11/beginners-guide-forex-scalping.asp.

Will Kenton. (2024). Flash Crash: Definition, Causes, History. [Online]. Investopedia. Last Updated: 21 May. Available at: https://www.investopedia.com/terms/f/flash-crash.asp#toc-examples-of-flash-crashes

{kind=link}