Abstract

This article examines the multifaceted impact of high-frequency trading, also known as HFT, on market stability, focusing on both traditional financial markets and the emerging landscapes of cryptocurrency. Beginning with a brief introduction about HFT, the article then delves into a literature review of articles named “The Impact of High-Frequency Trading Latency on Market Quality”, “The Impacts of High-Frequency Trading on the Financial Markets’ Stability”, and “High Frequency Trading, Stock Volatility, and Price Discovery”. In the body paragraph, we continue the topic by explaining the algorithms of HFTs, the impacts of HFTs on traditional financial markets and cryptocurrency, manipulative practices, impacts on the market of HFTs, a 2010 case study of a flash crash related to HFT, and regulatory frameworks along with examples for a more in-depth explanation.

1. Introduction

1.1 What is HFT?

HFT is short for high-frequency trading, a trading method that involves using powerful computer programs to transact a large number of orders in fractions of a second. HFT uses advanced computer algorithms and powerful technology to analyse market data, identify trading opportunities, and execute trades faster than any human possibly could. Key characteristics of HFT include speed, algorithmic strategies, high volume of trades, low holding periods, and requirement of infrastructure and technology. Impacts of HFT on the market include liquidity and narrow bid-asking spreads, which can make the markets more efficient. However, it can also lead to increased volatility and has been linked to flash crashes, where markets experience sudden and extreme price movements. Debates about HFT are often related to its ethics, particularly concerning its role in market fairness and the potential for manipulative practices like flickering quotes (rapidly placing and cancelling to create false signals). Common HFT use cases include equities and stocks, foreign exchange, derivatives trading, and cryptocurrencies.

1.2 Evolution of HFT

The birth of today’s HFT came in 2005 when the Securities and Exchange Commission (SEC) carried out major regulation alterations, decentralising exchanges and opening up arbitrage opportunities across exchanges. The use of advanced algorithms allowed the possibility to exploit price differentials across exchanges, capturing market inefficiencies and allowing firms to generate massive profits in milliseconds. Technological advancement in data processing, algorithmic computing, and low-latency networks has revolutionised trading, giving HFT firms the competitive edge over traditional traders. In recent years machine learning and AI have allowed sophisticated algorithms to learn from historical data, analysing vast data patterns invisible to humans, and making informed decisions with minimised market fluctuation risks. HFT is still in its early stages relative to traditional trading with its future anticipated to be impacted by: quantum computing development, providing enhanced computational power; blockchain and DeFi, providing a secure, efficient trading environment alternative to traditional financial markets; and potentially most significant, regulatory changes to ensure stability, efficiency and fairness across markets.

1.3 Market Efficiency

Market efficiency refers to the ability of a given market to accurately price all publicly known information, in such a way that opportunities arise solely from the analysis of said information. It stands at the core of any marketplace and economic system. In a purely theoretical world, without any human intervention, the price would always be correct, though the more speculation and guesswork influence the market, the more the price is affected, deviating from the original “correct” price. In this paper, we will analyse the effects of HFT algorithms in order to observe the changes, if any, they cause to the intrinsic price.

1.4 Market Stability

Market stability is the measure of how stable the environment is that the financial markets operate in. A market is deemed stable if it is able to respond to rapid, large-volume trades that are being exchanged every second. Prices of shares must also be consistent as well as there being an existence of an equilibrium between supply and demand. It is imperative to recognise that due to the number of trades taking place, unexpected market dynamics can be observed. To determine whether a market is stable or not, we would consider factors such as volatility, liquidity provision, and risk management. This will be explored in much greater depth in this academic paper.

2. Literature review

i. “The Impact of High-Frequency Trading Latency on Market Quality”

This article is focused on the outcomes that HFT can impose on different subtopics within market quality, such as liquidity and volatility (Ogunsakin, 2015). Before we evaluate any further, latency in HFT is defined as the time delay between the initiation of a trading signal and when the trade is carried out (Ogunsakin, 2015). An idea has been laid out throughout the article that HFTs can play a significant role in today’s financial markets, allowing for liquidity and helping with price formation while also engaging with ethical concerns such as speed and manipulative practices.

This article researched an objective i.e. how latency can impact key market quality factors as discussed above (Ogunsakin, 2015). Many approaches can be taken but this article has chosen the path of visualisation through mathematical modelling and simulation models. An example of Simulation Models used in the article are known as Discrete-Event Simulation (DES) and Agent-Based Simulation (ABS). In the context of this article, DES was used to simulate the trading procedures (Ogunsakin, 2015), focusing on the intricate sections like how often there were order submissions and how each of the events were timed. ABS was used to simulate the behaviour of individual investors (Ogunsakin, 2015) which includes both HFTs and manual traders.

Its key findings were that latency can help drastically improve liquidity by restricting bid-ask spreads (Ogunsakin, 2015). Bid-ask spreads are the difference between the highest price that the buyer will pay and the lowest price that the seller will accept. It could also introduce short-term volatility because of how rapid the trading times are; however, HFT can adapt rapidly to the market to help stabilise prices. One of the most crucial findings of this article was that latency helped with price discovery (Ogunsakin, 2015), i.e. lower latency allowed for HFTs to exploit opportunities while observing price changes. Its overall findings were that although HFTs can impact volatility, these can be recognised as bad short-term impacts. However, we should note that an overall positive impact can be made on the market.

ii. “The Impacts of High-Frequency Trading on the Financial Markets’ Stability”

This paper analyses the implications of HFT on market quality but additionally and most significantly, stability in relation to volatility and systemic risk. HFT has become a dominant component of modern financial markets, now accounting for over 50% of trading volume in the US which gives it major influence over market quality, reducing bid-ask spreads and contributing to price efficiency. However, it has also been associated with increased market volatility such as the 2010 flash crash (Hamza, 2015).

The key thesis of this paper highlights the impacts of HFT on market stability and the mixed impact on volatility. An idea intrinsic to the paper is the mixed impact of HFT on volatility, often enhancing liquidity and price efficiency in normal market conditions; however, under periods of market stress it can act as a destabilising power (Hamza, 2015), most clearly highlighted through the 2010 flash crash which will be evaluated later in our paper. The paper investigates the liquidity provisions from HFT, underlining the idea that HFT generally improves liquidity which contributes to market stability, however, key emphasis must be put on the fact that liquidity disappears during volatile periods when necessitated. A key argument of this paper is the fact algorithmic HFT is underlying to short-term volatility with rapid trading and frequent order cancellation, including sudden withdrawal of liquidity by HFT firms inherent to serve price swings and destabilisation, leading to brief volatility spikes which affect market stability (Hamza, 2015).

Furthermore, the paper sees systemic risk relating to the utilisation of HFT due to the interconnected nature of the algorithmic systems, amplifying shocks and potentially triggering widespread disruptions across markets. Algorithmic errors or rapid market movements speed quickly creating a path to systemic failures (Hamza, 2015). The general conclusions of the article were that while HFT enhances market efficiency and liquidity in normal market conditions, this benefit is overridden by the conjunction of short-term volatility spikes during periods of stress, the systemic risk of algorithmic failure, and the fragility of liquidity in volatile markets. Thus, without careful regulatory oversight, HFT pose detrimental implications for the future stability of financial markets.

iii. “High-Frequency Rrading, Stock Volatility, and Price Discovery”

This paper looks at the correlation between stocks, especially high-cap stocks, with high HFT activity and their respective volatility, measured by the magnitude of price swings. Moreover, the study poses the question of whether high-frequency trading helps facilitate or impede price discovery. The dataset is very large, spanning almost three decades of information, from 1985 to 2009. The timeframe is very important, as it looks at the years in which HFT became more and more prevalent, incorporating data from the times in which high-frequency trading was barely used to the years in which 70% of the trades were made by such algorithms (Zhang, 2010). The study finds that volatility is positively correlated with HFT activity, showing that these algorithms increase volatility by 30% on average, reaching 40% for the already volatile stocks (Zhang, 2010).

On the other hand, the paper also proves quite an important upside, showing that HFT makes price discovery 1.5 times faster on average, and two times faster for the already volatile stocks. Though, Zhang (2010) shows that high-frequency trading algorithms tend to overestimate the impact of new information leading to a slight deviation from the “correct” price. The study concludes that because of the increased volatility, high-frequency trading warrants careful regulation, while also highlighting the importance of letting the industry grow as it also provides liquidity and faster price discovery. Also, the authors call for a need for continuous and new research on the topic, as well as policy discussions to find better ways in which to keep the benefits of HFT’s upsides, while capping the downsides to a minimum.

3. HFT’s Impact on Traditional Financial Markets and Price Discovery

3.1 Changes in market liquidity and order size

In the context of any financial market, investors will always try to find new and innovative ways to make more returns on their investments. The High-Frequency Trading industry is no exception. By 2005, 20% of all equity trading in the US was made by such algorithms, this number continued to rise, up until 2009, when it peaked at 60% (DB Research,2016). A considerable majority of the market consisted of software trying to gain an edge simply by being the fastest, not the smartest or the best informed.

Both stock and derivatives exchanges have begun to let companies in the business of algorithmic trading move directly into their headquarters, for a price, in order to give said companies the same proximity to the servers (DB research, 2016). Thus, it can be understood that these exchanges promote algorithmic trading, but is this justified? While High-Frequency Trading does provide liquidity, making the most out of its market-maker properties, it occupies quite an aggressive and large part of the total volume of trading and it is “clearly excessive if HFT is meant to provide liquidity” (Zhang, 2010). This does reduce the cost of trading for most participants of the market though, as a large order split into multiple smaller ones is harder to identify, thus making a lesser impact on the price, which in turn reduces the bid-ask spread (D. Murphy, 2013). Furthermore, market makers would charge a smaller commission for multiple smaller trades, as a larger trade will come with more financial complications for said market maker. This additional cost would be passed onto the regular investor, who must now pay the bid-ask spread, plus a small part of this increased cost (D. Murphy, 2013). This phenomenon of splitting large transactions into multiple smaller ones has been steadily on the rise, thus reducing the operational costs of all market participants. The average size of a buy or sell order in 1997 was 5600 shares, while in 2009 it fell sharply down to 400 (D. Murphy, 2013). Furthermore, in the same time span, the average number of consecutive buy or sell orders rose from 2.3 to 11.9, a 417% increase (D. Murphy, 2013). This serves as proof of the impact of high-frequency trading and change in general trading behaviour, while also highlighting the increase in retail traders prevalent for the past few years.

3.2 Changes in market efficiency and price discovery

After understanding the changes in liquidity caused by high-frequency trading algorithms, we must now address the changes in market efficiency, focusing mostly on the topic of price discovery and high-frequency trading algorithms’ impact on them. First and foremost, it is important to note that these programs have “no intrinsic interest in the fate of companies, leaving little room for a firm’s fundamentals to play a direct role in its trading strategies” (Zhang, 2010). This goes against the fundamental ideology that stands at the core of price discovery, in which investors rely on information and analysis to trade, thus helping the price reach a “fair” equilibrium. When outliers of this principle, such as high-frequency trading algorithms appear on the market, it tends to mess up this otherwise sound system, as such programs rely mostly on speed and statistical, short-lived correlations as the basis for their transactions (Zhang, 2010).

Though, high-frequency trading amounts to a very big part of the price reaction seen after a major news breakout, being responsible for “70% of price reactions in the first ten seconds following a news release” (Martinez and Rosu, 2013). Moreover, stocks with high HFT activity incorporate new information 1.5 times faster than stocks with low HFT activity (Zhang, 2010). Although, all these benefits do come at a cost, derived also from the increase in liquidity that these algorithms provide; the cost is the increase in volatility. To be exact, Zhang finds that high-frequency trading increases short-term intraday volatility by 30%. This makes it riskier for any traditional investors, while also raising the prices of derivatives that rely on volatility, such as options. Furthermore, Zhang implies that incorporating new information into the price quicker leads to an over-exaggeration in price swings post a news release. This is understandable as programs can copy one another, leading to many orders being placed all at once, thus changing the price rapidly, though often past its “correct” price.

3.2.1 The differences of price discovery in regular stocks and in stocks with high HFT activity

Additionally, Zhang presents a difference between the fluctuation of already volatile stocks and regular ones, presenting a two times faster price discovery and a 40% increase in volatility. Moreover, the same study presents a unique discovery. High HFT activity decreases market depth by 15%, meaning that there are fewer shares to be traded beyond the best quotes. There is another problem though: HFT software is only active during normal market conditions. This means that during times of market stress and uncertainty, liquidity provided by HFT is decreased by 40% (Brogaard et al., 2014) and spreads can widen by an average of ten basis points, unwinding their previous tightening of five basis points, during regular periods.

3.3 The efficient allocation of resources in relation to HFT

Market efficiency can also be interpreted as the efficient allocation of resources, for the betterment of the overall environment, for both investors and market makers. In this regard, Nanex – Exhibit A (2011) shows that because of the thousands upon thousands of orders caused by HFT algorithms, the cost to store and process the data has skyrocketed. The study mentioned above shows a graph of how many quotes it takes to transact $10,000 worth of stock in the US, taking its data from 535 billion quotes and 35 billion trades over 1,172 days. The conclusion is that because of the increased HFT activity in the past few decades, stock exchanges will have to pay their data providers at least ten times more for said data brokers to upgrade their storage to be able to store the enormous number of additional quotes caused by such algorithms. This cost is once again passed onto regular investors, who do benefit from increased liquidity and usually tighter spreads, but also have to bear the risk of increased volatility and possible liquidity runs in periods of market downturn.

4. HFT Impacts on Cryptocurrency Markets

4.1 Implications and Impacts of Cryptocurrency in HFT

Implications and impacts of cryptocurrency in HFT include its high volatility that creates ample opportunities for HFT strategies. Unlike traditional markets, cryptocurrency markets operate 24/7, which can provide continuous trading opportunities. This constant market availability is ideal for HFT firms to execute trading at any time. The decentralised nature of cryptocurrencies also leads to fragmented markets. HFT can capitalise on price discrepancies between these platforms through arbitrage strategies, though it requires sophisticated infrastructure to manage different exchanges. Since cryptocurrencies operate in a less regulated environment compared to traditional financial markets, it allows more aggressive HFT strategies which introduces uncertainties around legal and regulatory compliance, especially as governments around the world develop new rules for digital assets.

4.2 Examples of Different Cryptocurrencies

- Bitcoin: Bitcoin is the most liquid cryptocurrency and it plays a central role in high-frequency trading. It has a massive daily trading volume across numerous exchanges, ensuring that it can be executed quickly and efficiently without causing significant price fluctuations.

- Ethereum: Ethereum is another major player in the HFT space due to its substantial liquidity and high trading volume. The cryptocurrency’s support for smart contracts allows HFT strategies to automate trading processes and execute complex transactions based on predefined criteria. It has significant price volatility that provides opportunities for HFT firms to profit from short-term price movements.

- Stablecoins: Stablecoins, such as Tether (USDT) and USD Coin (USDC), are essential tools in HFT for managing risks and facilitating trades. Related to traditional currencies such as the USD, stablecoins offer a stable value, which is crucial for trading in volatile markets. Their stability allows HFT firms to efficiently move in and out of more volatile assets. Additionally, stablecoins are widely used as base pairs on cryptocurrency exchanges, providing high liquidity and enabling rapid trading and arbitrage.

4.3 Future of Cryptocurrency

The future of cryptocurrency in relation to HFT is poised to be dynamic and transformative, driven by technological advancements, regulatory developments, and the increasing institutionalisation of the crypto market. As cryptocurrencies continue to evolve, they are expected to play a more prominent role in HFT strategies, reshaping the financial landscape in several key ways.

The technological advancements and innovations in the future, such as blockchain upgrades, would likely reduce transaction times and fees, making them more conducive to HFT. It could also allow HFT algorithms to execute trades with reduced latency, which is crucial for maintaining a competitive edge. It is also estimated that there will be increased institutional participation in the future. As the trend of increasing institutional investors entering the cryptocurrency market will likely continue in the future, the overall liquidity of cryptocurrencies is expected to increase. It means that HFT firms can execute larger trades without significantly impacting market prices.

As AI and machine learning have been developed and improved significantly recently, it is also predicted that AI and machine learning will be integrated into HFT strategies that could revolutionise cryptocurrency trading. These technologies can analyse vast amounts of market data in real time and identify patterns that human traders might miss. AI-driven HFT strategies could also become more adaptive over time, learning from market conditions and adjusting trading parameters to maximise profitability. Machine learning algorithms could also be used to predict market movements based on historical data and macroeconomic indicators (Power, 2024).

Although it is impossible to predict exactly what will happen to the crypto market in the future, there are a few crucial details that should be focused on: regulation in the US and abroad, mass-market adoption of cryptocurrency payments, exchange-traded funds based on Bitcoin and other digital currencies, and countries adopting Bitcoin or other digital currencies as legal tender (Bylund 2023). Some have argued that cryptocurrency could be the future of money as the international viewpoint for crypto starts to change. For example, El Salvador and the Central African Republic view Bitcoin as an official currency (Bylund 2023). Furthermore, governments have started to develop regulations related to cryptocurrency that could allow it to be used on a large scale. Many stores and retailers are also starting to accept payment through digital currency such as Bitcoin, Litecoin, or Dogecoin. Although the change for cryptocurrency to be more widely accepted is likely to be a long process, there are definitely small consistent improvements throughout time.

5. Manipulative Practices and its Impact on the Market

Manipulative practices are quite an important aspect of HFTs to consider, especially when monitoring market quality. HFTs make use of algorithmic trading which takes up about 70% of total trading volumes (Hanson et al., 2013) of securities such as stocks, futures, and derivatives. There are many arguments when considering what is ethical and not ethical in trading, and one of these is the Low Trade-to-Order Submission Ratios (Hanson et al., 2013). It is imperative to note that rapid and high-volume trades have a great number of transactions occurring; however, some trading algorithms generate orders and then cancel them immediately, providing the illusion that the stock is high in demand. There are about 20-25 orders that are made for each execution (Hanson et al., 2013) by the algorithm. This can be used in favour of the trader, but there can be arguments that this can have a positive impact on the market like market making. This is the process of continually providing bid-ask prices and can allow for liquidity to improve in the long term.

Large companies that make use of HFTs can invest in machines that provide a speed advantage for receiving data through optical fibre links; as opposed to normal trading, where people would use their eyes, this can be argued as receiving information quicker. Now, in the context of HFTs when computers are running algorithms, a huge difference can be made in milliseconds. Another sector of significant value is the slow market arbitrage (Hanson et al., 2013), i.e. the market is not able to respond and adjust to price changes so HFTs can take advantage of this using prediction techniques in machine learning to give a higher probability of obtaining a profit. Fictitious trades are considered a dangerous technique (Hanson et al., 2013), but they can increase the volume of shares. The key thing to note is that the ownership of the underlying assets (Hanson et al., 2013) does not alter and this is strictly prohibited by the SEA. This will be explored in detail, looking at concepts like spoofing alongside price manipulation, which is again disallowed by SEA.

Price manipulation is such that the price of a stock is altered (Hanson et al., 2013) to then lure others to buy it, which can negatively impact investor sentiment. This can be done using AI, i.e. algorithmic trading, so it is of great difficulty to prove the intent of the user, making it near impossible to pursue legal action. However, it is interesting to observe that there is still an ongoing debate; an ideal solution would recognise “fictitious trades as species of fraud” (Hanson et al., 2013). This can be argued, as intent should not matter, but if we were to put a line through these types of trading techniques, then it would make the market a much fairer place. There seems to be a lack of evidence to suggest, however, that market manipulation can pose harmful effects to the market; though evidently it will bring positive impacts to individual traders that can build small profits rapidly.

This paragraph will explore the details of the strategies before we delve into the impacts that they can pose on market quality. Firstly, one must emphasise that arbitrage trading can help improve liquidity. It involves purchasing and then selling an asset at the same time with a price difference (Hanson, Kashyap and Stein, 2013) to make a profit. It takes advantage of rapid price variations and even if very little money is made, it would contribute to a bigger amount in the long term. We can start discussing a “manipulative” strategy known as quote stuffing. This is commonly used and stuffs quotations with useless orders (Hanson, Kashyap and Stein, 2013), essentially acting as an obstacle and, as time is of the essence, this can be used to the advantage of other traders. It may seem like a simple method but it can have a drastic effect on other traders.

Let us discuss layering and spoofing now. Layering was discussed earlier when orders are constantly stacked and when full, will be calling on other traders for purchases (Hanson, Kashyap and Stein, 2013) while simultaneously cancelling the orders. It is an attempt to alter the trend of a stock to then create confusion amongst algorithms. This is very similar to spoofing, but this is the most common jargon for HFT startups. Its strategy is to initiate orders and withdraw immediately before execution (Hanson, Kashyap and Stein, 2013) as an attempt to trick the market into buying the shares by artificially inflating the volume of the orders. At surface level, this does not seem ethical at all, but with the lack of research showing drastic effect to others, this does not seem to be recognised as advantageous in any aspect. If anything, there are more positive effects because market manipulation can allow for more HFTs to trade greater volumes of securities (Hanson, Kashyap and Stein, 2013) and therefore would lead to less market abuse. They will buy and sell unlike humans which would encourage liquidity, i.e. the desired outcome or factor to be considered when evaluating market quality, and allow for more employment and lower trading costs for investors (Hanson, Kashyap and Stein, 2013). Although this seems unethical, it does pose a plethora of benefits for all.

There are some exceptions of course, when considering historical events such as the Flash Crash of 2016 where the DJI fell to its lowest in history. This was recovered in only minutes but evidence showed that HFT was responsible for these rapid price fluctuations as there was a sell-order for $4.1 billion (Hanson et al., 2013).

These techniques were explored in depth but now let us evaluate whether market quality can change. HFT traders require stocks of low price and large liquidity (Li, 2018), and designing different algorithms can provide for the ability to recognise that liquidity can be consumed at different times of the market. This type of trading has evidence to support the claim that the liquidity that is provided is like the amount that it is consumed (Li, 2018), essentially being at an equilibrium. Also, if a market is volatile, then traders will exit the market automatically allowing for market quality to recover to its original state, ensuring that it does not worsen. This is quite a crucial point to observe.

Previously, we mentioned that there are fewer worsening impacts from HFTs, but we must note that when they exist, they tend to be quite drastic. Large numbers of trades are generated in short time intervals and with the use of deceptive tactics (Li, 2018), volatility can substantially change. This is again how the 2016 Flash Crash occurred. HFT is synonymous with volatility in the sense that it is one of the most predominant causes of volatility in today’s financial markets.

Before we discuss the more “aggressive” strategies, we would like to emphasise that actions can be considered as unethical by inspecting the outcome. This is another reason why regulation is required in today’s markets. This will be explored in further detail, at a policy level, later in the paper.

There have been numerous efforts to stop manipulative methods such as spoofing. It is imperative to observe the alterations in the Commodity Exchange Act to prohibit methods such as spoofing with intent and violations in bids or offers (Dumont, 2016). Loopholes are opened through the mention of the word “intent” as we cannot justify intent when an AI is performing such an action as opposed to a human making their own decisions. But, if we constrain it to repeatedly cancelling an offer before execution (Dumont, 2016), then we are able to see true intent and therefore can enforce a ban.

Many HFTs can perform this technique but it would not be considered under the category of “spoofing” because of the number of algorithms performing such an action (Dumont, 2016). Therefore, when taking legal action, there must be strong evidence to show that the intent of the trader was to manipulate the market in their favour, even if there are positive outcomes. Michael Coscia, owner of a proprietary energy trading firm, was convicted on accounts of spoofing (Dumont, 2016) after this new alteration in the HFT law, and this shows how strict action can prevent further use of manipulative methods.

To conclude this section on manipulative techniques, it is necessary to note that manipulative methods can be removed through strict regulation but it is imperative to bring awareness to all traders of what is allowed and what isn’t. This can be done through strict and rigid definitions, rather than “liquid” rules that have loopholes in them. The world of HFT is evolving, where traders can all have an equal playing ground.

6. The Role of Regulation in Managing Impact of HFT on Market Stability

6.1 Case Study: 2010 Flash Crash

The 2010 Flash Crash was a market crash and partial rebound over the space of an hour on May 6th, 2010. The result of the crash saw US stocks including the Dow Jones, S&P 500, and Nasdaq have a net loss of over $1 trillion of market value. While high-frequency trading was not the full, direct cause of the crash, it played a major role in creating the circumstances available for such a crash to occur and for the extent of the crash to be so large. While the day of the crash was underlined by volatility in not only stocks but futures, options and ETFs, the cause of the crash was determined by the SEC and CFTC as a sell program from Waddell & Reed Financial Inc. to sell a total of 75,000 E-Mini S&P contracts, while disregarding time or price of sales during execution. This was defined as the cause of the crash; however, the circumstances over the following minutes, predominantly by HFT algorithms created the necessity for the regulatory framework to control HFT, protecting market stability.

High-frequency trading firms rapidly began buying and then quickly offloading the contracts they had just bought from this sale to gain a rapid profit on the cut prices, but the volume of these sales kept pushing down prices by 3% in the space of four minutes. The buyers and other arbitrageurs who bought the contracts sold off stocks in the equities markets, pushing it down additionally by 3%. As algorithms rapidly noticed the dip, a major sell-off occurred as HFT bots tried to release contracts and shut off, however, the simultaneous similarities between firms meant the contracts were sold between each other. 27,000 contracts were traded in 14 seconds, accounting for 49% of trading volume, while buyers for the E-Mini dropped to $58 million, less than 1% of the level in the morning. This HFT-induced liquidity crisis led to another drop in price, and this gave a cross-market indication that there was a lack of supply of liquid assets leading to a decline of 6% to the SPY. Finally, after four and a half minutes, a five-second circuit break was put in to stop further price declines, but the damage was done. While prices rose over the next few minutes, unregulated HFT algorithms had contributed to a trillion-dollar stock market disaster.

6.2 Regulatory frameworks to increase market stability in HFT dominated markets

The evolution of high-frequency trading has been rapid and extensive, making up huge amounts of trading volumes and having a large impact on market stability and efficiency. With algorithmic development and trading speed rapidly improving, regulation has regularly failed to keep up, putting market stability at risk of volatility spikes, fragile liquidity, and systemic risk posed by trading. Regulation is currently a requirement with the goals of increasing transparency, developing stability, and halting manipulative practices entirely with the hope of never having a repeat of the damage caused by the 2010 Flash Crash.

Currently, regulations vary vastly across the world with no international oversight body. The most complete regulation exists in the European Union with the Markets in Financial Instruments Directive II (MiFID II), which is a complete and comprehensive regulatory framework directly targeting HFT as a protective act for market stability. MiFID II needs all firms engaging in HFT to be authorised, maintain digital records of trades, and ensure their trading algorithms do not contribute to market instability. Germany specifically goes further with the implementation of the High-Frequency Trading Act (2013), which has imposed stringent licensing requirements for HFT firms and additionally requires all forms to introduce circuit breaks into their algorithms for protection while also limiting the use of co-location servers (Crump, 2015). Co-location servers are used to reduce latency with proximity to exchange servers. These restrictions increase latency and execution time therefore removing some of the competitive advantage along with the short-term volatility risk in low liquidity markets.

The United States is also a major player, with HFT making up over 50% of trade volume; however, it has been slow to develop targeted regulation. Existing regulation such as the Market Access Rule (Rule 15c3-5) requires brokers to have risk management controls which indirectly sets a risk threshold that HFT traders cannot cross. Additionally, there are enforcement actions which target manipulative practices for HFT such as the aforementioned spoofing which creates major market volatility (Crump, 2015). Italy specifically has taken a novel approach to HFT regulation, levying a 0.02% tax on all trades occurring in under 0.5 seconds (Stafford, 2013) targeted at slowing trades, increasing latency, eliminating short-term volatility risks, and raising competitive fairness in traditional markets. The impact was almost instant, seeing a 30% drop in trading volume on the Milan index over a 90-day average along with volatility reduction, protecting the wider consumer base (Clinch, 2013).

While regulation is critical to halt market manipulation and events such as our case study of the 2010 Flash Crash, it comes with its own difficulties and risks, particularly when recognising truly illegitimate misconduct. Firstly, difficulty comes when regulators look to enact laws distinguishing between legitimate and illegitimate behaviours. High-frequency trading is based on innovative strategy, though activities such as market making and arbitrage, while both legitimate, are occasionally used to overshadow and conceal manipulation in forms such as spoofing. This HFT overlap makes the job for regulators exceedingly difficult to identify, regulate, and then prove misconduct without risking the threat of penalising legal trading practices (Cosme Jr. 2019). Secondly, HFT, for regulatory sake, is difficult to define, particularly when trying to hold firms to account for malpractice. The typical characteristics of high volumes of trades at speeds under a second also account for other forms of automated trading, now with technical and market innovations, able to be performed at home, while not being considered HFT. This blurry line of what high-frequency trading is makes it difficult for a regulator to effectively target reckless behaviours without overbearing frameworks threatening trading freedoms (Cosme Jr. 2019).

6.2.1 Specific HFT regulatory frameworks’ effect on market stability

6.2.1.1 Circuit Breakers

Two main types of circuit breakers exist currently in HFT regulation. Firstly, ex-ante exists as a mechanism that introduces a limit up/down price of a stock which, when triggered, halts all trading on the exchange for a fixed period which in turn, eliminates flash crash risks. An example of this is the Deutsche Boerse. Secondly, ex-post circuit breakers implement a stop to trades in single stockers, caused by a certain percent price change from the last price. The contrast in impact on market stability can most easily be seen through flash crash simulations under different frameworks where the average duration of flash crashes saw an 86% duration increase with ex-post from 7.14 to 13.36, while with the use of ex-ante, flash crashes’ duration dropped to zero as the total exchange stop eliminates the possibility of an HFT induced flash crash (Jacob Leal and Napoletano, 2016). This use of ex-ante circuit breakers, in turn, leads to a reduction in price volatility, increasing market stability.

6.2.1.2 Minimum resting times

In high-frequency trading, a minimum resting time is a rule that makes it illegal and technically impossible to cancel or change an order until some amount of time has elapsed from its submission. The necessity for this regulation to protect market stability is due to the risk of high-frequency trading algorithms cancelling orders, giving a short-term, misleading image on market liquidity, implying an increase and creating information asymmetry, leading to favourable short-term volatility for high-frequency trading bots and the chance to capitalise on beneficial prices. The utilisation of minimum resting times also creates an openness for market participation as slower market speeds mean wider access to small retail investors without HFT speed or volume capabilities.

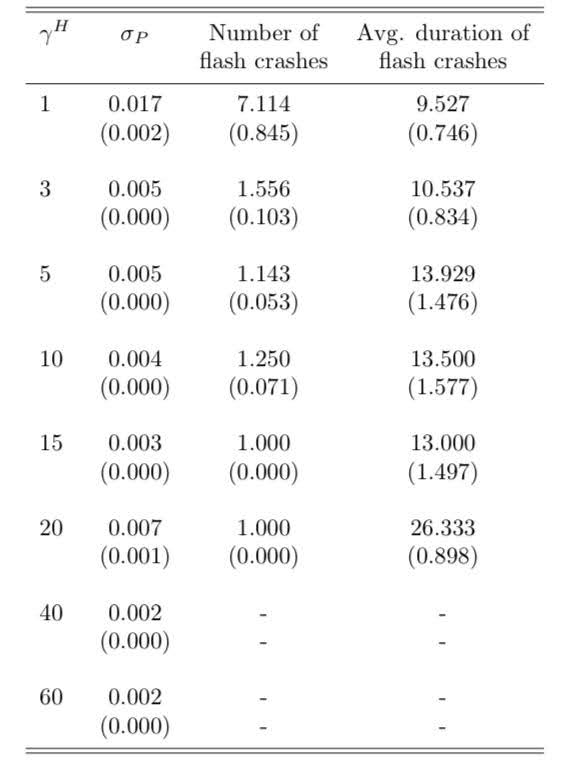

Figure 1: Chart showing data pertaining to the impact of minimum resting times on flash crashes. (Market Stability vs. Market Resilience: Regulatory Policies Experiments in an Agent‐Based Model with Low‐ and High‐Frequency Trading)

As the chart indicates, minimum resting times have crucial impacts on market volatility and therefore protect trading stability. Utilising a Monte-Carlo experiment for HFT orders under different periods (expiration time) from 1 to 60 periods/minute, an increase in minimum resting time (gamma H) results in a reduction in market volatility (column 2) resulting in primarily a decrease in number of flash crashes. This does come with slight increases in the duration of flash crashes, however, the fact that at 40 or more periods/min resting time, flash crashes are eliminated and, excluding the outlier at 20, there is clear evidence that an effective regulatory framework implementing minimum rest periods elevate market stability, reduce flash crash induced volatility spikes, and protect low-frequency traders (Jacob Leal and Napoletano, 2016).

6.2.2 Volatility comparison with differing regulatory frameworks

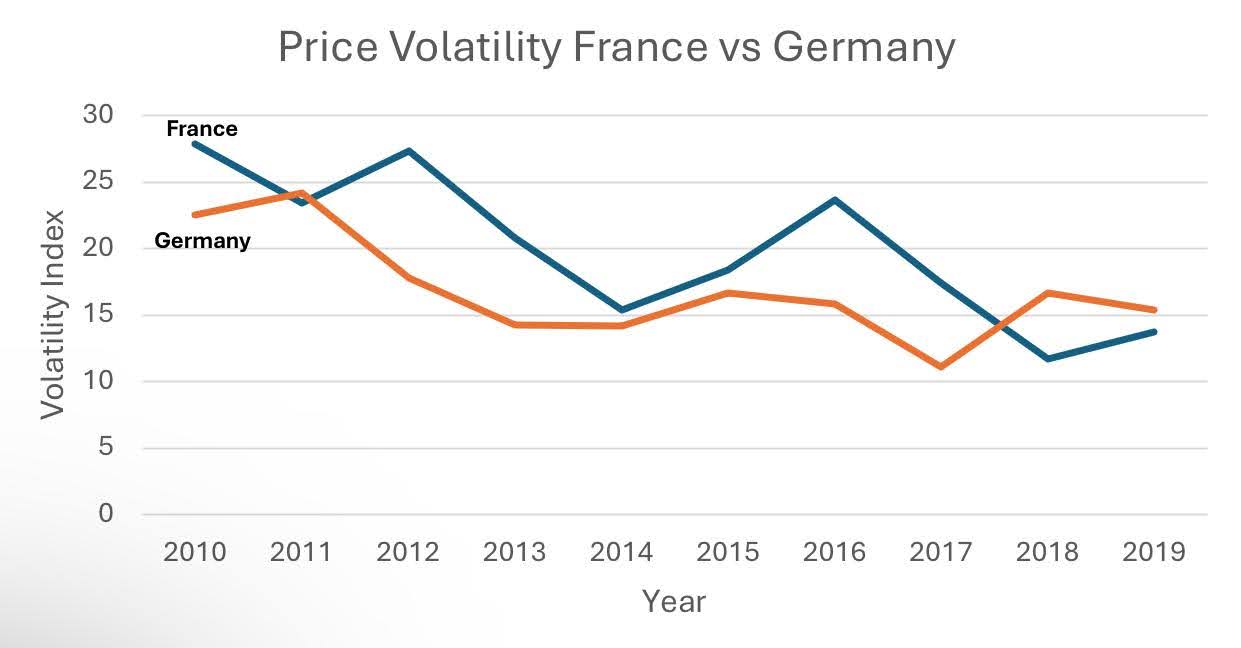

| Year | France Volatility Index | Germany Volatility Index |

| 2010 | 27.85 | 22.55 |

| 2011 | 23.46 | 24.20 |

| 2012 | 27.36 | 17.80 |

| 2013 | 20.78 | 14.23 |

| 2014 | 15.41 | 14.18 |

| 2015 | 18.41 | 16.67 |

| 2016 | 23.63 | 15.83 |

| 2017 | 17.38 | 11.09 |

| 2018 | 11.67 | 16.64 |

| 2019 | 13.72 | 15.39 |

Figure 2: Chart showing a comparison of price volatility in countries with differing regulatory frameworks.

Figure 3: Graph illustrating comparison of price volatility in countries with differing regulatory frameworks. (Federal Reserve Bank of St Louis)

Standard deviation is calculated to compare volatility variability which creates a further level of market unpredictability. The equation, where: 𝝈 is the standard deviation; ∑ is the sum; xi is the first number in the data set; 𝜇 is the mean; and N is the total number of values, is:

𝝈=√(∑(xi-𝜇)^2/N)

- 𝜇 volatility France: 19.97

- 𝜇 volatility Germany: 16.86

- 𝝈 France: 5.60

- 𝝈 Germany: 3.49

Data Interpretation

France has a higher average volatility index (19.97) than Germany (16.86) over the period of 2010-2019, along with a higher standard deviation of volatility, indicating that France’s stock market experiences higher variability in volatility compared to Germany. The significance of this data is that it indicates the beneficial impacts of higher levels of HFT regulation on market volatility in comparable countries due to both having approximately 50% of trading volume from HFT. Both France and German traders are compliant with MiFID II, however, the significance of the German HFT act, including ex-ante circuit breakers, creates a more sheltered market in Germany which dampens the impacts of flash crashes and produces increased stability. To conclude, Germany’s proactive utilisation of specific HFT targeted regulatory framework contributes to its relative lower market volatility and mitigates the risks of HFT; therefore, contributing to a more stable market environment in comparison to France.

7. Conclusion

This paper concludes that the impacts that HFTs can impose is a complex issue with both positive and negative outcomes for financial markets. It has rapidly altered traditional markets by increasing liquidity, reducing bid-ask spreads, and allowing for rapid price discovery. However, the transition to a computer from a human has also introduced significant risks, including heightened volatility, potential price manipulation, and increased systemic risk, as seen by events such as the 2010 Flash Crash. It has also brought up the need for a change in regulatory framework in order to constrain certain types of manipulative practices as an attempt to make the market fair for all.

Bibliography

Bylund, A., 2023. Future of Cryptocurrency. The Motley Fool. Available at: https://www.fool.com/investing/stock-market/market-sectors/financials/cryptocurrency-stocks/future-of-cryptocurrency/ [Accessed 19 August 2024].

Clapham, B., 2023. The Impact of High-Frequency Trading on Modern Securities Markets. Available at: https://link.springer.com/article/10.1007/s12599-022-00768-6#:~:text=The%20results%20of%20Hasbrouck%20and,lower%20short%2Dterm%20price%20volatility [Accessed 31 August 2024].

Clinch, M., 2013. Italy launch tax on high-frequency transactions. Available at: https://www.cnbc.com/id/101002422# (Accessed: 29 August 2024).

Cosme Jr, O., 2019. Regulating high-frequency trading: the case for individual liability. Available at: https://scholarlycommons.law.northwestern.edu/cgi/viewcontent.cgi?article=7648&context=jclc (Accessed: 29 August 2024).

Crump, L.C., 2015. Regulating to Achieve Stability in the Domain of High-Frequency Trading. Mich. Telecomm. & Tech. L. Rev., 22, p.161. Available at: https://repository.law.umich.edu/cgi/viewcontent.cgi?article=1214&context=mttlr.

Deutsche Bank Research, 2016. Research briefing: High-frequency trading. Frankfurt am Main: Deutsche Bank AG. Available at: https://www.dbresearch.com/PROD/RPS_EN-PROD/PROD0000000000454703/Research_Briefing_High-frequency_trading.pdf (Accessed: 31 August 2024).

Dumont, C., 2016. Government-Owned, Contractor-Operated (GOCO) Model at the National Laboratories. Congressional Research Service. Available at: https://sgp.fas.org/crs/misc/R44443.pdf [Accessed 19 August 2024].

Federal Reserve Economic Data, 2024. Volatility of Stock Price Index for France/Germany. Available at: https://fred.stlouisfed.org/series/DDSM01FRA066NWDB, https://fred.stlouisfed.org/series/DDSM01DEA066NWDB (Accessed: 30 August 2024).

Hamza, H.R., 2015. The impacts of high-frequency trading on the financial markets’ stability (Master’s thesis, Kent State University).Available at: https://etd.ohiolink.edu/acprod/odb_etd/ws/send_file/send?accession=kent1428416050&disposition=inline [Accessed 21 August 2024].

Hanson, S., Kashyap, A. and Stein, J., 2013. Market Manipulation Case Study. Harvard University. Available at: https://projects.iq.harvard.edu/files/financialregulation/files/market_manipulation_case_study.pdf [Accessed 19 August 2024].

Jacob Leal, S. & Napoletano, M., 2016. Market Stability vs. Market Resilience: Regulatory Policies Experiments in an Agent‐Based Model with Low‐ and High‐Frequency Trading. Available at: https://www.ofce.sciences-po.fr/pdf/dtravail/WP2016-12.pdf (Accessed: 29 August 2024).

Li, B., 2018. Ethical Reflections on High-Frequency Trading. Journal of Business and Economics, 9(6), pp. 518-525. Available at: https://www.davidpublisher.com/Public/uploads/Contribute/5b1a2dbbe1a79.pdf [Accessed 19 August 2024].

Madonna, L., 2017. High-Frequency Trading: Overview of Recent Developments. Seven Pillars Institute. Available at: https://sevenpillarsinstitute.org/wp-content/uploads/2017/11/Laure-Madonna-High-Frequency-Trading.pdf [Accessed 19 August 2024].

Martinez, Victor & Rosu, Ioanid. (2013). High Frequency Traders, News and Volatility – Invited Talk. SSRN Electronic Journal. 10.2139/ssrn.1859265.

Murphy, D., 2013. The Impact of High-Frequency Trading on Stock Market Liquidity Measures. Available at: https://elsevier-ssrn-document-store-prod.s3.amazonaws.com/13/07/22/ssrn_id2297073_code1778503.pdf (Accessed: 31 August 2024).

Ogunsakin, R.S., 2015. An investigation into the performance analysis of composite materials using finite element method. MSc dissertation. University of Manchester. Available at: https://studentnet.cs.manchester.ac.uk/resources/library/thesis_abstracts/MSc15/FullText/Ogunsakin-RotimiSamuel-diss.pdf [Accessed 18 August 2024].

Powers, J., 2023. AI Trading: How AI Is Used in Stock Trading. Built In. Available at: https://builtin.com/artificial-intelligence/ai-trading-stock-market-tech [Accessed 19 August 2024].

Stafford, P., 2013. Italy introduce tax on high-speed trade and equity derivatives. Available at: https://on.ft.com/3T1YvTw (Accessed: 30 August 2024).

U.S. Securities and Exchange Commission (SEC), 2010. Findings regarding the market events of May 6, 2010. Available at: https://www.sec.gov/news/studies/2010/marketevents-report.pdf (Accessed: 30 August 2024).

Zhang, S., 2010. High-frequency trading, stock volatility, and price discovery. Available at: https://elsevier-ssrn-document-store-prod.s3.amazonaws.com/10/12/26/ssrn_id1731384_code343637.pdf (Accessed: 31 August 2024).

{kind=link}