Abstract

This paper explores the transformative impact of Financial Technology (FinTech) on the real estate industry, focusing on AI-driven property valuation, digital lending platforms, and smart contracts. By integrating these technologies, the real estate market benefits from enhanced efficiency, accessibility, and accuracy. AI and big data have revolutionised property valuation by offering deeper insights and more precise assessments, thus aiding both investors and buyers. Digital lending platforms have streamlined mortgage processes, making credit more accessible to a broader demographic, including first-time buyers and those with non-traditional credit profiles. Smart contracts, powered by blockchain technology, further streamline real estate transactions by automating agreements, reducing transaction costs, and enabling fractional ownership through tokenisation.

However, these advancements also introduce challenges. Data privacy and security concerns must be addressed to safeguard sensitive information. The ease of obtaining digital loans necessitates careful regulation to prevent over-leveraging and financial instability. Legal and technological hurdles for smart contracts require clear regulatory frameworks and robust security measures to ensure reliability and broad adoption.

1. Introduction

Financial Technology (FinTech) has been disrupting and innovating financial markets since the 2008 financial crisis, in particular, changing old ways of working that hindered progress and success. Outdated methods of working requiring manual data collection and analysis have been replaced with tools in the 21st century to be able to focus on the microscopic detail that can be extracted from a vast macro perspective on data. This can be seen with the use of AI in real estate, which has allowed investors to have access to enormous amounts of data to be then able to make use of analytical skills to capitalise on industry advantages to make the shrewdest acquisitions ahead of others, using comparisons provided by AI. Digital lending means that the barriers to accessing funds have been drastically removed, opening up investment opportunities to a much wider consumer range. Smart contracts further reduce the barriers to investment, allowing first-time buyers and large-scale investment firms to access properties much faster than before, and increasing the housing allocation rate, which can also help in social aspects.

As with any technological implementation, there are also concerns surrounding data security and market stability. These are some key factors to explore as to whether FinTech is an overall net positive or negative for investors and whether it is possible to implement on a wider scale due to the large-scale initial investment required to implement these fintech tools and the cost associated with maintaining their integrity.

2. Literature Review

This research paper focuses on whether an investor, specifically in real estate, should adopt the use of financial technology. Many recent studies have focused on the difficulty of buying property in the UK. While there has been substantial research into FinTech, few researchers have yet to explore the idea of implementing FinTech into the real estate sector to make the process of buying and selling housing easier.

Fitzpatrick (2023) theorises that Generative Artificial Intelligence (Gen AI) can and will have a huge impact on the housing market, and mentions that based on work by the McKinsey Global Institute (MGI), Gen AI could potentially generate $110 to $180 billion or more in revenue for the real estate industry. Several studies have focused on the future of artificial intelligence and its possible use cases (Zhang et al.,2021; Shabbir & Anwer, 2018a). A research paper by Uke (2014) confirmed a relationship between the future uses of artificial intelligence and the real estate market, particularly in real estate forecasting.

Artificial intelligence has the ability to refine and even improve current, long-standing real estate tactics. This can be done by integrating artificial intelligence’s powerful summarisation and research capabilities. However, since the complete capabilities and limitations of artificial intelligence are still unknown, the literature could overlook the niches and nuances of the real estate market and the possible challenges that artificial intelligence implementation may present.

The Federal Reserve Bank of Philadelphia (2019) proposes that digital or FinTech lenders will expand the mortgage market. By 2017, about 1 in 10 mortgages originated by FinTech firms, which is theorised to be due to FinTech lenders giving mortgages to people not usually served by traditional lenders. Multiple studies have concentrated on the growth of FinTechs and their potential for the future, such as McKinsey & Company (2023). Moreover, a research paper by Freddie Mac (2019) creates a link between the use of FinTech and the satisfaction and ease of transactions for customers, which ultimately leads to more mortgages being provided.

Digital lending by FinTech companies could expand the mortgage market. This would be done by appealing to more customers, who either are overlooked by traditional mortgage brokers, or are hesitant because they feel the mortgage process could be more seamless and efficient. However, the literature overlooks the huge proportion of people choosing to use traditional means to broker a mortgage over digital lending. This could be due to mistrust of digital lending or simply habit and comfort in a conventional mortgage broker.

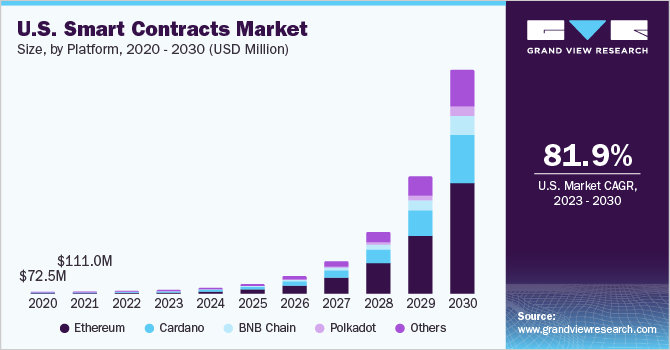

World Economic Forum (2024) theorises that smart contracts will have a large impact on the housing market and projects that, by 2030, the smart contracts market should reach $73 billion due to a compound annual growth rate (CAGR) of 82.2%. While several studies have highlighted the prosperous future of smart contracts, such as Bird & Bird (2021), a study by IEEE Xplore (2024) demonstrates a clear link between the possibilities available with smart contracts and the applications then available in the real estate market.

3. The Role of AI and Big Data in Real Estate Valuation

Real estate investors in the modern era can look to the use of FinTech to gain an advantage in their knowledge and comprehension of the property market compared to other agencies and investors, due to FinTech being able to process and analyse vast amounts of data in an ever-evolving and digital market. For example, this can be done by comparing listing prices of properties across similar criteria, by compiling data from websites that hold sales data, to be able to come to a fair valuation for a property price in the market. Continually, investors would be able to use FinTech to check if the price they are being touted for a property is viable in a similar way, by being able to use AI to compile sales data for properties using key criteria such as its location, lot size, amenities, and floor plan, which are key to valuations. By using AI to run through databases, one can find comparable properties to the one being sold/bought, which then forms the basis for negotiations. This would give investors a negotiation advantage against sellers, as they are able to do vast amounts of research in a much shorter time. Therefore, entering negotiations for a property then becomes much easier, as they have the benefit of close-to-perfect information on the property they are interested in. Otherwise, the seller would be at an advantage due to asymmetric information against the investor.

3.1 Generative AI and Discrete Analysis

Investors can make great use of generative AI in their field by way of concision. Investors can use generative AI to look at large-scale data through a macroanalysis lens from in-house databases on sales data, and other data, or other digital tools such as Zoopla in the UK. This then allows investors to conduct more discrete analyses to whittle down their findings to be relevant to the necessary property criteria. For a large-scale investment firm, this type of tool would be vital to be able to beat the competition to the best possible purchases, not only in smaller-scale housing but also large-scale commercial sites such as offices. By being able to see such a large amount of data for comparable properties, the investor in charge of the discrete analysis can use their industry experience to conclude on the best opportunity to then invest in, based on their historical knowledge of the market. Historically, success in real estate came from having large amounts of liquid cash and an intricately vast contacts list of both buyers and sellers to be able to get ahead of others. However, the implementation of AI results in the same race for success but in a different way. Expertise and the necessary insight to analyse the data given is now a large part of being able to get the edge over others, who will have similar tools to help analyse data but may need more expertise to act upon it. This is the best example of how FinTech can be used to aid investors in the modern day to keep up with a much more digital market. While the strong presence of AI increasingly exists to make investing in real estate “easier” by way of research and analysis opportunities, an investor with expertise is still needed to get to the opportunities the quickest. Therefore, while the barriers to compete have been lowered, this does not guarantee success for everyone.

3.2 Challenges and Risks

However, the use of generative AI in real estate comes with its challenges, such as the need for large-scale upfront investment to gain access to these tools in some aspects, although online real estate markets do exist, which makes this easier. Furthermore, although one may have access to this data, anyone looking to invest as a new investor with little to no experience in the market will still have to look to a FinTech consultant for help, which then harms their ability to move as fast as others, meaning they lose any advantage they may have had by using FinTech. Whilst the use of FinTech is clearly a benefit to investors, there are some underlying issues with using an unregulated AI tool to access the sensitive data of thousands of transactions, as well as market stability by having wide-scale access to these tools.

The main argument against the use of FinTech is the data protection concerns around using such vast amounts of personal transaction data, which needs to be thoroughly regulated. The world of finance has gone from inefficient manual workstreams to a massively digital workspace, which has become a target for cybercriminals. Personal identity information, financial records, and transaction details are all being stored by FinTech companies. Therefore, data breaches are far more likely than in the past. Phishing scams, leaks, and attacks are a threat to the use of FinTech in real estate due to the personal nature of the market. This can be extremely harmful to the argument for the use of FinTech on a wider scale, as not everyone that may choose to use a tool will have the necessary cybersecurity to justify its use. The use of FinTech requires compliance with the General Data Protection Regulation (GDPR) to maintain client privacy and trust. Still, some argue that more is needed, as customers are at risk of not only misuse of data from the company itself but also cybercriminals. It could be argued as to whether it is a net positive or negative to use FinTech in real estate when considering the required costs and regulations associated with keeping data safe.

3.3 Impact on Market Stability

Furthermore, it has to be acknowledged that since the 2008 Financial Crisis, over 25,000 FinTech startups have been started worldwide. This means that the market will be flooded with investors and data that has yet to be made available. Therefore, the stability of the market can be questioned as the demand for property drastically increases beyond the supply, affecting the valuation and price of the properties, alongside such a massive increase in the information available to investors. This can be seen to disrupt and cause a decline in the appetite of buyers, as uncertainty breeds an environment where people are more likely to save. This means that such an unstable market can harm both buyers and sellers, who are then less likely to be able to access the required resources. Furthermore, it causes a negative multiplier effect on other aspects of the economy if house prices and sales do not act accordingly, potentially harming those who need a house or those needing to sell. This causes a lack of supply for investors, as tenants may not want to sell into an uncertain market, which in turn makes the use of FinTech less applicable. On the other hand, sellers may see this as an evening of the playing field. Despite these concerns, FinTech is a massive net positive for investors and those who are able to use it. The increased number of buyers drives up the price for the seller, which means that they are not being exploited and are able to raise their asking price accordingly.

3.4 Real Estate Valuation Through AI

The use of FinTech for investors has an overall net positive effect, despite concerns around the legal and moral issues, which can be dealt with to gain access to the massive benefits and advantages it can provide. The sheer amount of data that can be compiled and analysed completely changes and reinvents what the market may look like, with much lower barriers to entry and more emphasis on the analysis of what FinTech can provide. The concerns around the wider use of market stability and data security are issues that can be dealt with through compliance with GDPR and other regulatory bodies, which will work to maintain customer safety while allowing investors, as well as customers themselves, to benefit, through potentially higher prices due to increased competition for securing high-value property.

4. Mortgage Tech and Digital Lending

Financial technology has revolutionised numerous industries, with mortgage lending being one of the most significantly impacted industries. Digital lending platforms have not only streamlined the mortgage process, but have also made financing more accessible to a broader segment of the population. This transformation promises to alleviate some of the most pressing issues in the housing market, particularly for first-time buyers and those traditionally excluded from accessing credit. However, the rise of FinTech in mortgage lending has its new challenges, particularly in terms of consumer protection, market stability, and regulatory oversight. This section of the paper provides an in-depth analysis of the strengths and challenges posed by FinTech innovations in mortgage lending. It examines their potential impact on the housing market, considering the lessons from the 2008 Financial Crisis to ensure a stable and equitable real estate market. The analysis also focuses on the UK’s current housing crisis, exploring how FinTech can contribute to both alleviating and exacerbating existing problems.

4.1 The Rise of Digital Lending Platforms

The traditional mortgage process is often seen as slow, complex, and cumbersome, with a heavy reliance on in-person interactions and extensive documentation. FinTech has disrupted this landscape by introducing digital lending platforms that provide a more streamlined and user-friendly experience. These platforms have become increasingly popular due to their ability to offer faster approvals and more flexible options for borrowers. A report by the Federal Reserve Bank of Philadelphia found that FinTech mortgage lenders process loans 20% faster than traditional lenders, with no increase in default rates. This efficiency is largely due to the use of sophisticated algorithms that analyse a wide array of data points to assess credit risk beyond the traditional FICO scores. These data points include social media activity, spending patterns, and even utility payment histories. A study by the Cambridge Centre for Alternative Finance (CCAF) highlighted that digital lenders are more likely to approve loans for individuals with non-traditional employment or limited credit history, a demographic often underserved by traditional banks.

Moreover, the scalability of digital lending platforms enables them to serve a larger and more diverse customer base. According to a report by McKinsey & Company, as of July 2023, there were more than 272 FinTech unicorns, with a combined valuation of $936 billion, a sevenfold increase from 39 firms valued at $1 billion or more five years ago. This growth is driven by the increasing adoption of digital banking services, particularly among younger, tech-savvy consumers, who prefer the convenience and speed of online transactions.

4.2 Automated Underwriting and Real-Time Decision Making

Automated underwriting is a key FinTech innovation that has revolutionised the mortgage approval process. Traditional underwriting methods are labour-intensive and time-consuming, often taking weeks to complete. In contrast, automated underwriting systems use machine learning and big data to evaluate a borrower’s creditworthiness in real time. These systems can analyse vast amounts of data, including non-traditional financial indicators, allowing for a more nuanced assessment of risk. Research by the National Bureau of Economic Research (NBER) found that automated underwriting systems reduce the likelihood of human error and bias in the loan approval process, resulting in more accurate and equitable lending decisions. The study also noted that these systems have increased mortgage approval rates for minority borrowers, who have historically faced discrimination in the traditional mortgage market. By reducing the reliance on subjective judgement, automated underwriting helps ensure that borrowers are evaluated based on their true financial health rather than stereotypes or outdated criteria.

Furthermore, the speed and efficiency of automated underwriting have significant implications for the housing market. Quicker approvals mean that buyers can secure financing faster, which is particularly advantageous in competitive housing markets where properties sell quickly. A report by Freddie Mac indicated that the average time to close a mortgage has decreased in markets where digital lending is prevalent. This reduction in processing time can make a significant difference for buyers and sellers alike, facilitating smoother and faster transactions.

4.3 Blockchain and Smart Contracts in Mortgage Tech

Blockchain technology has the potential to further disrupt the mortgage industry by enhancing transparency, security, and efficiency. At its core, blockchain is a decentralised ledger that records transactions across a network of computers, ensuring that the data is immutable and transparent. This technology can be particularly beneficial in the mortgage industry, where the process is often opaque and prone to fraud. Smart contracts, which are self-executing contracts with the terms of the agreement directly written into code, represent a significant innovation in mortgage tech. These contracts can automate various aspects of the mortgage process, from the initial agreement to the final payment, reducing the need for intermediaries and lowering transaction costs. According to a report by Deloitte, the use of blockchain and smart contracts could reduce mortgage processing costs by up to 20% and cut down processing times by more than 50%.

Moreover, blockchain technology can enhance the security of mortgage transactions by providing a tamper-proof record of ownership and transaction history. This increased security is particularly important in preventing fraud, which remains a significant issue in the mortgage industry. A study by the International Monetary Fund (IMF) noted that blockchain could play a critical role in reducing the incidence of mortgage fraud by creating a transparent and immutable record of transactions.

4.4 The Impact on the Housing Market

4.4.1 Addressing the Accessibility Gap

One of the most significant benefits of digital lending platforms is their potential to increase accessibility to mortgages for underserved populations. Traditional mortgage systems often exclude individuals with non-standard employment, limited credit history, or lower incomes. Digital lending platforms, however, can assess a broader range of financial behaviours, and therefore offer mortgage products to a more diverse group of borrowers. Digital lending platforms have a higher approval rate for minority and low-income borrowers compared to traditional banks. This increased accessibility is crucial in addressing the significant homeownership disparities that exist in many markets, including the UK. According to The Institute for Fiscal Studies, the last 20 years have seen a substantial fall in homeownership among young adults. By making mortgages more accessible, digital lending can reverse this trend and help more people achieve homeownership.

Furthermore, digital lending can play a crucial role in expanding access to affordable housing. The Financial Times reported that the UK needs to build at least 500,000 new homes each year to meet demand – larger than the 300,000 target from both main political parties – with a significant portion of these homes needing to be affordable for low- and middle-income families. Digital lenders can support this effort by providing financing options tailored to first-time buyers and those seeking affordable housing, thereby helping to address the supply-demand imbalance in the housing market.

4.4.2 Potential Risks and the Lessons from 2008

While the benefits of digital lending are clear, it is essential to acknowledge the potential risks associated with this technology. The 2008 Financial Crisis reminds us of the dangers of inadequate regulation and poor lending practices. The crisis was precipitated by the widespread issuance of subprime mortgages, many of which were poorly underwritten and offered to borrowers who ultimately could not afford them. As a result, default rates soared, leading to a collapse in the housing market and a global financial meltdown.

The rapid proliferation of digital lending platforms raises concerns about the potential for similar issues to arise. If automated underwriting systems are not sufficiently transparent, or if lending standards are relaxed in the pursuit of market share, there is a risk that digital lending could lead to a new wave of consumer over-leveraging. The ease with which loans can now be obtained online might lead to an increase in risky borrowing behaviour, particularly among younger and less financially literate consumers. Moreover, the algorithms used in automated underwriting are not infallible. While they are designed to reduce bias and improve accuracy, they can also perpetuate existing inequalities if not properly monitored. A report by the Centre for Financial Inclusion highlighted that algorithms could inadvertently reinforce discriminatory practices if they rely on biased data, or if the criteria used to assess creditworthiness are not carefully calibrated. Therefore, it is crucial to ensure that these systems are transparent, fair, and subject to regular oversight.

4.4.3 Impact on the Current UK Housing Crisis

The UK is currently grappling with a severe housing crisis characterised by soaring property prices, a shortage of affordable homes, and significant regional disparities in housing availability. Depending on how it is implemented and regulated, digital lending has the potential to both alleviate and exacerbate these issues. There are also potential downsides to the increased accessibility of credit. If the supply of housing does not keep pace with the increased demand facilitated by digital lending, property prices could continue to rise, further exacerbating the affordability crisis.

Nevertheless, on the positive side, digital lending can help more people enter the housing market, particularly first-time buyers who often struggle to secure financing through traditional means. Digital lending offers more flexible mortgage products and faster approval processes, which enables a broader range of people to achieve homeownership. This can increase homeownership rates, particularly among younger and lower-income households.

5. Smart Contracts in Real Estate

5.1 Definition of Smart Contracts

A smart contract is a digital program integrated within the blockchain that is able to enforce the terms of a contractual agreement without the help of an extra third party. Pioneered by Nick Szabo in the 1990s, the idea behind the use of smart contracts was to establish a “peer-to-peer market” between the client and supplier. The blockchain is the most critical and essential part of the process, as each step, from the primary marketing to the final transaction, takes place on its network. Primarily, a supplier will reach out to its potential clients via a catalogue, disclosing information such as the property, price, quantity, etc., along with shipping and payment terms to verify the supplier’s credentials and the authenticity of the potential transaction. Once the client is ready to purchase a product from the supplier, the person will submit their payment date and the amount needed/wanted from the supplier. These details will form a primary purchase contract enclosed in a specific box on the blockchain. A third party does not intervene when this takes place. Once this primary purchase contract concludes, a secondary and final purchase contract is ushered in. This consists of many of the same elements as seen in the primary contract, including shipping details and terms and shipping conditions sent by the carrier to the supplier; all of these details, like the first contract, are enclosed in a box on the blockchain. Once the supplier accepts the terms and conditions posed by the carrier, the products will then be sent to the carrier, who will then send them to the client. Once again, this all proceeds without the intervention of a third party. The primary and secondary contracts are not the only aspects of this model that are executed automatically; the payments and financial operations conducted in cryptocurrency (i.e., Bitcoin or Ether) are also automatically completed. The exclusion of third parties, such as banks, allows for a peer-to-peer market system with decreased turnaround times and transactional fees.

5.2 Relevance of Smart Contracts in Real Estate

Closing a process takes place after a house is no longer taking offers from others and has found clientele that either outbid or has purchased for the agreed-upon price, which, according to Investopedia, typically follows twelve long and tedious steps to ensure fairness for all parties on the sides of the transaction. The twelve steps are opening an escrow account, confirming the title and acquiring title insurance, hiring an attorney, negotiating costs, home inspections and pest inspections, renegotiating your original offer and acknowledging the interest rate, removing contingencies, meeting the financial requirements, completing a final walk through, and then finally completing the paperwork and closing the house. It takes roughly 30 to 45 days to close a house, according to Investopedia; that is a month or more of time spent on a piece of property.

Now, a response to the prior statement would fall along the lines of: “Rightly so, ownership of property is a significant milestone in any individual’s lifetime. The process should be tedious and thorough to ensure that this person is not cheated out of this impactful moment”. That is a consideration that is important to keep in mind; however, in this rapidly modernising and advancing world, the market that possesses the ability to give the consumer their wants or needs in the shortest time holds a significant sum of power within that sector of the market.

Take companies like Amazon, an enterprise that profits off its ability to give you the convenience of its service by shipping goods to you quickly. Note how the process of traditional transactions between the buyer, seller, third party, etc., not only further draws out the process in which one purchases a home but also contributes to the overall expenditure for the potential buyer looking to finance a home. Suppose you modernise the real estate market to become convenient, efficient, and fast by utilising the blockchain and smart contracts. In that case, the client has the option to cut out administrative fees and excess expenditures. This, in turn, makes it easier to purchase a home while also saving the consumer a significant portion of their capital.

5.3 Components of Smart Contracts in Real Estate

A great aspect of the current blockchain system is that transaction programs already exist for consumers and producers. An Engineering, Technology and Applied Science Research article discusses the existence of Block Estate, a platform set to transform the real estate industry by utilising the transactional properties of the pre-existing Hyperledger platform on the blockchain. Due to the program’s decentralised, immutable, and transparent technologies, a consumer worried about fraud will not only have the option of legal and regulatory justice, but the chances of being cheated out on a sale will be significantly lowered because of these features.

Another venue that the digitisation of properties and their ownership allows for is the tokenisation of land. This provides investors with an easy and efficient way to buy and sell property without actually having to set foot on the property in the first place.

According to the article Smart Contracts and Tokenisation: Revolutionising Real Estate Transactions with Blockchain Technology (which describes the process in which real estate tokenisation would follow), a platform known as Blockrealty, which uses the Ethereum platform (another vetted program on the blockchain, much like Hyperledger), could be used for transparent and secure transactions in the real estate sector digitally. When looking to purchase a property (or a fraction of one), this program will automatically write a smart contract known as the ERC-721. The ERC-721 is a standard real estate tokenisation contract with three steps to secure transactions and guarantee they are not compromised while purchasing. Buyers, lenders, inspectors, and sellers oversee all of the three steps. The ERC-721 smart contract then converts the asset or assets into a token or tokens, known as NFTs (Non-Fungible Tokens). In addition, the system uses IPFS (InterPlanetary File System), which safeguards property images and metadata via a decentralised storage system. Finally, the program exploits the Metamask to make the program user-friendly and easy to navigate.

Let’s say, however, that you currently need to possess the capital to buy a whole property or are an investor wanting to test these new waters. Then, this program could provide another, less volatile venue known as fractional ownership. This is definitely possible. Rae Hartely Beck from Bankrate lists the types of properties that can be fractionally owned, including hotels, companies, and yachts, among other assets. Once the program takes off, this option could be not only a possibility but also a way for more investors to get into the real estate business, which typically benefits all parties. Finally, a big question one may ask is: “Is this even legal?”. The answer to this is most certainly yes. The UK Jurisdiction Taskforce puts it best: “In legal terms, crypto-assets and smart contracts undoubtedly represent the future”, and the article Regulating Smart Contracts: Legal Revolution or Simply Evolution? describes smart contracts as “the intersection of technology and law”. While it is safe to say that the legality of smart contracts cannot inherently come under fire, legislators may find ways to support or undercut the action in future years.

5.4 Use Cases of Smart Contracts in Real Estate

Now understanding the basic components and technologies of smart contracts, we can explore property sales and purchases, rental agreements, real estate crowdfunding, and land title management. We can also understand what said functions do and how they intertwine with smart contracts. One of the most obvious ways smart contracts can benefit the real estate sector is in the realm of quick, digital sale deals. As mentioned previously, smart contracts underpin a new system that ensures fast and secure transactions, specifically in the sphere of property purchasing. Saving time is a greatly impactful added benefit of this system and will be described in further detail in the paper. Access to an escrow account and the safeguarding of the wealth until the purchase is agreed upon is another benefit escrow services on the blockchain and, as smart contracts already exist, a paper called XRP Ledger describe the benefits of using this system. They write how, by using the smart contract as an escrow account, the third party or oracle never actually “holds” the funds.

Thus, capital cannot be stolen and fraud can be combatted. What makes this system even better is that the oracle is the smart contract, therefore eliminating the hypothetical third party. The smart contract works like the account in the way that it holds the cryptocurrency, the only difference being that it cannot release the currency until the pre-written commands are executed, and the parties typically set these prerequisites. Are you still deciding whether to become a homeowner yet? Renting can be made easy with the introduction of smart contracts as well. Just as purchasing arrangements can be automated, so can rental contracts. This automation follows much of the same code. However, paying rent would be different, such that a perpetual smart contract would bill the tenants, the frequency of which is set by the landlord.

LinkedIn contributor, Towfik Alrahizi, describes the components and process of smart contracts in detail in the following sentences. The components of a rental smart contract would be the Ethereum addresses of both the landlord and tenant, the deposit in Ethereum, the duration of the lease, and boolean flags (boolean meaning boolean logic: a type of algebra classifying data as TRUE or FALSE with the help of tools called truth variables). In this case, the boolean flags are “is Active” and “is Terminated”. The tenant is meant to enact the “pay Rent” command with the correct amount owed and update the contract. The landlord would then “terminate Contract”, the command returning the stake to the tenant after the duration of the lease. The enforcement of these terms would likely not be automated since the landlord would be able to see if the amount had been paid. If not, an eviction notice may be placed over the tenant until the amount owed is given.

The distribution of wealth or crowdfunding is an important consideration for an investor looking into any form or sector in which to invest. Nasdaq reports that a special type of model is used when approaching crowdfunding with smart contracts, which is known as a milestone-based funding model. Unlike traditional investments that demand money upfront with little guarantee that the investment will return when promised, a smart contract is altered in said model, such that the code incrementally hands out funds based on the milestones reached by the invested company. This way, management and the investor can rest easy knowing that the function of paying out dividends was done effectively and on time. A person at this point may be wondering where the title gets transferred in all of this. Certain smart contracts and land management agencies on the blockchain may provide a way to secure this final step of acquisition. An article titled Blockchain-based Secure Land Registry System using Efficient Smart Contract describes how, with the use of specialised web pages, smart contracts can be deployed by the Ethereum network while the page takes care of the rest of the routing and transfer functions. Smart contracts fully automate the process of buying properties digitally, and it does this with fewer steps and in a fraction of the time of traditional home purchasing.

6. Conclusion

The integration of financial technology (FinTech) in real estate, driven by AI, big data, and smart contracts, signifies a transformative shift in the industry. It offers substantial benefits while also posing challenges that require careful management.

6.1 Advantages and Innovations

AI and big data have revolutionised property valuation by providing deeper and more accurate analyses of market trends and economic indicators. Unlike traditional methods, these technologies analyse extensive datasets to deliver precise valuations, benefitting both buyers and investors by reducing information gaps and enhancing decision making. Digital lending platforms have streamlined the mortgage process, making it faster and more inclusive. By leveraging non-traditional data sources, these platforms extend access to credit for a broader range of borrowers, including those with unconventional employment or limited credit histories. This improved accessibility supports homeownership, particularly for first-time buyers and underserved communities. Blockchain technology enables smart contracts, which further enhance the efficiency of real estate transactions. These self-executing agreements automate processes, reduce reliance on intermediaries, and lower transaction costs. By eliminating administrative fees and expediting the buying and selling process, smart contracts make real estate transactions more efficient and accessible. Additionally, the tokenisation of real estate assets facilitates fractional ownership, allowing more individuals to invest in property.

6.2 Challenges and Risks

Despite their benefits, FinTech innovations present several challenges. The use of AI and big data raises concerns about data privacy and security. Ensuring compliance with regulations, such as GDPR, and safeguarding sensitive information is critical to maintaining trust and protecting against cyber threats. Additionally, data-driven models must be scrutinised to prevent biases that could affect valuation and lending decisions. While digital lending platforms make mortgages more accessible, they also introduce risks. The ease of obtaining loans could lead to over-leveraging if not properly regulated. It is essential to maintain transparency and adhere to responsible lending practices to prevent financial instability. Smart contracts face legal and technological hurdles. The legal framework for smart contracts is still developing, with varying levels of acceptance across jurisdictions. Ensuring the security and reliability of smart contracts is vital to prevent cyber threats and programming errors. Clear regulatory guidelines and ongoing technological advancements are necessary for effective implementation and broader adoption.

6.3 Potential for Further Innovation

The potential for continued innovation in real estate through FinTech is significant. Advancements in AI could lead to even more precise valuation models and predictive analytics, improving decision making. Blockchain technology and smart contracts will likely evolve to offer greater transaction efficiencies, cost reductions, and security. Digital lending platforms are also expected to advance, providing more tailored and accessible financing options. Balancing these innovations with regulatory oversight will be crucial to ensuring market stability and consumer protection.

6.4 The Future of Real Estate

FinTech is set to significantly shape the future of real estate by enhancing efficiency, transparency, and inclusivity. Addressing the associated challenges through effective risk management and regulatory compliance will be key to harnessing these technologies’ full potential. By doing so, the real estate market can embrace these advancements to create a more equitable industry.

Bibliography

Acemoglu, D. & Restrepo, P. (2018). Artificial Intelligence, automation and work. National Bureau of Economic Research. doi:https://doi.org/10.3386/w24196. (Accessed: 20 August 2024).

Beck, R.H. (2022). What is fractional ownership?, Bankrate. Available at: https://www.bankrate.com/real-estate/fractional-ownership/ (Accessed: 31 August 2024).

Cambridge Judge Business School. (2024). The future of global FinTech: Towards resilient and inclusive growth – CCAF publications – Cambridge Judge Business School. [online] Available at: https://www.jbs.cam.ac.uk/faculty-research/centres/alternative-finance/publications/the-future-of-global-fintech-towards-resilient-and-inclusive-growth (Accessed 20 Aug. 2024).

Clarke, A. (2023). Smart contracts and crowdfunding: Redefining Investment Opportunities, Nasdaq. Available at: https://www.nasdaq.com/articles/smart-contracts-and-crowdfunding:-redefining-investment-opportunities (Accessed: 31 August 2024).

Cribb, J. and Simpson, P. (n.d.). Barriers to homeownership for young adults © Institute for Fiscal Studies 1 9. Barriers to homeownership for young adults. [online] Available at: https://ifs.org.uk/sites/default/files/output_url_files/GB9%252520-%252520housing%252520pre-release%252520-%252520final%252520from%252520Judith.pdf. (Accessed 21 August 2024).

Deloitte (2017). Blockchain in real estate. Available at: https://www2.deloitte.com/content/dam/Deloitte/us/Documents/financial-services/us-dcfs-blockchain-in-cre-the-future-is-here.pdf/ (Accessed 21 August 2024).

Discover thousands of collaborative articles on 2500+ skills (no date) LinkedIn. Available at: https://www.linkedin.com/pulse/exploring-rental-agreement-smart-contract-towfik-alrazih (Accessed: 31 August 2024).

Ferreira, A. (2020). Regulating smart contracts: Legal revolution or simply evolution?, Telecommunications Policy. Available at: https://www.sciencedirect.com/science/article/abs/pii/S0308596120301713 (Accessed: 31 August 2024).

Fitzpatrick, M. et al. (2023). Generative AI can change real estate, but the industry must change to reap the benefits, McKinsey & Company. Available at: https://www.mckinsey.com/industries/real-estate/our-insights/generative-ai-can-change-real-estate-but-the-industry-must-change-to-reap-the-benefits (Accessed: 23 August 2024).

Folger, J. (2024). What you should know about real estate valuation, Investopedia. Available at: https://www.investopedia.com/articles/realestate/12/real-estate-valuation.asp#:~:text=Key%20Takeaways%201%20Real%20estate%20valuation%20takes%20into,estimate%20of%20the%20present%20value%20of%20future%20benefits. (Accessed: 23 August 2024).

Freddie, M. (2019). Digital mortgages: How leaders are harnessing tech to streamline processes, cut costs and improve customer experience. Available at: https://sf.freddiemac.com/docs/pdf/other/freddie-mac-future-of-lending.pdf/ (Accessed: 21 August 2024).

Grand View Research (2023). Smart contracts market size, Share & Analysis Report, 2030 (no date) Smart Contracts Market Size, Share & Analysis Report, 2030. Available at: https://www.grandviewresearch.com/industry-analysis/smart-contracts-market-report (Accessed: 31 August 2024).

IEEE Xplore. (2024). Available at: https://ieeexplore.ieee.org/Xplore/home.jsp (Accessed: 31 August 2024).

International Monetary Fund (2022). Blockchain consensus mechanisms: A primer for supervisors. Available at: https://www.imf.org/en/Publications/fintech-notes/Issues/2022/01/25/Blockchain-Consensus-Mechanisms-511769/ (Accessed: 21 August 2024).

Jugtiani, J. et al. (2019). Fintech Lending and Mortgage Credit Access. The Federal Reserve Bank of Philadelphia.[online] Available at: https://www.philadelphiafed.org/consumer-finance/mortgage-markets/fintech-lending-and-mortgage-credit-access (Accessed 20 Aug. 2024).

Kessler, A. & Menajovsky, J. (2024). Reducing bias in algorithmic decisions cannot rely on “blind” approaches. Centre for Financial Inclusion. Available at: https://www.centerforfinancialinclusion.org/reducing-bias-in-algorithmic-decisions-cannot-rely-on-blind-approaches/ [Accessed 21 August 2024].

Klein, M. (2022). What boolean logic is & how it’s used in programming, Codecademy Blog. Available at: https://www.codecademy.com/resources/blog/what-is-boolean-logic/ (Accessed: 31 August 2024).

McKinsey & Company (2023). Fintechs: A new paradigm of growth | McKinsey. [online] McKinsey & Company. Available at: https://www.mckinsey.com/industries/financial-services/our-insights/fintechs-a-new-paradigm-of-growth. (Accessed: 20 August 2024).

Naz, L.F. et al. (2024). Blockestate: Revolutionising real estate transactions through Hyperledger-based blockchain technology, Engineering, Technology & Applied Science Research. Available at: https://etasr.com/index.php/ETASR/article/view/7105 (Accessed: 31 August 2024).

Reiter, A., Murray, C. and Oliver, J. (2024). How many homes does England really need to build? [online] www.ft.com. Available at: https://www.ft.com/content/32846f68-52fd-40e1-9328-0fe6bb3b9c19. (Accessed: 21 August 2024).

Seth, S. (2024). 12 steps of a real estate closing, Investopedia. Available at: https://www.investopedia.com/articles/mortgages-real-estate/10/closing-home-process.asp#toc-how-long-does-it-take-to-close-on-a-house (Accessed: 31 August 2024).

Shabbir, J. & Anwer, T. (2018a). Artificial Intelligence and its role in the near future. arXiv.org. Available at: https://arxiv.org/abs/1804.01396 (Accessed: 30 August 2024).

Sharman, J., & Kukadia, P. (2021). Smart contracts – recognising and addressing the risks. Bird & Bird. Available at: https://www.twobirds.com/en/insights/2021/uk/smart-contracts-recognising-and-addressing-the-risks (Accessed: 31 August 2024).

Square Mile (2024). Why Fintech is the future of Real Estate, Square Mile. Available at: https://squaremile.com/property/fintech-future-real-estate/ (Accessed: 23 August 2024).

Team, N.F.V. (2022). The emergence of FinTech in real estate transactions, Nine Four Ventures. Available at: https://ninefour.vc/2022/08/26/the-emergence-of-fintech-in-real-estate-transactions/ (Accessed: 23 August 2024).

Uke, N. (2014). http://citeseerx.ist.psu.edu/viewdoc/download?doi=10.1.1.401.8095&rep=rep1&type=pdf, Academia.edu. Available at: https://www.academia.edu/6390087/http_citeseerx_ist_psu_edu_viewdoc_download_doi_10_1_1_401_8095_and_rep_rep1_and_type_pdf (Accessed: 30 August 2024).

World Economic Forum (2024). The rise of smart contracts and strategies for mitigating cyber and legal risks World Economic Forum. Available at: https://www.weforum.org/agenda/2024/07/smart-contracts-technology-cybersecurity-legal-risks/ (Accessed: 31 August 2024).

XRP Ledger (2024). Use an escrow as a smart contract. XRP LEDGER. Available at: https://xrpl.org/docs/tutorials/how-tos/use-specialized-payment-types/use-escrows/use-an-escrow-as-a-smart-contract (Accessed: 31 August 2024).

Zhang, C., & Lu, Y. (2021). Study on Artificial Intelligence: The state of the art and future prospects. Journal of Industrial Information Integration. Available at: https://www.sciencedirect.com/science/article/abs/pii/S2452414X21000248 (Accessed: 30 August 2024).

Zheng, Z. et al. (2019). An overview on smart contracts: Challenges, advances and platforms, Future Generation Computer Systems. Available at: https://www.sciencedirect.com/science/article/abs/pii/S0167739X19316280 (Accessed: 31 August 2024).

{kind=link}