Abstract

The purpose of this research paper is to examine the relationship between the dollar cycle, emerging markets and financial stability. Global organisations such as the IMF and the World Bank play an important role in supporting developing countries through financial assistance and policy advice, but their assistance is denominated in dollars and is dependent on the dominance of the US dollar, which can create problems. This paper examines the implications of currency dominance, focusing on the role of the US dollar in supranational organisations and geopolitical leverage, such as sanctions. Dollar fluctuations not only affect the policies of multiple countries, but also determine global financial conditions. The process of de-dollarisation has already begun, however, and new dominant currencies such as the Chinese yuan and the Indian rupee have emerged.

1. Introduction

In an increasingly interconnected global economy, the role of the US dollar as the dominant global currency has far-reaching implications for emerging markets and worldwide financial stability. The dollar’s status not only shapes international trade dynamics, but also monetary policies and economic growth trajectories in developing economies. Understanding the impact of the US dollar cycle on these markets is crucial, as such fluctuations in its value can lead to significant economic consequences including inflationary pressures and heightened vulnerability to external shocks. This research paper aims to explore the multifaceted relationship between the US dollar cycle, emerging markets, and global financial stability, shedding light on the mechanisms behind the rise and fall of global currencies and some of the challenges faced by developing nations.

Supranational organisations such as the International Monetary Fund (IMF) and the World Bank play a prominent role in the global financial system, particularly in supporting developing or underdeveloped economies. These institutions provide financial and technical assistance, alongside policy recommendations to countries facing economic adversities. The IMF focuses on short- and medium-term loans whereas the World Bank focuses on long-term development projects. Nonetheless, both organisations heavily rely on the US dollar’s dominance, as the financial assistance provided by both is denominated in dollars, which can create challenges for developing countries that lack the ability to print their own currency. While relying on the dollar allows for the establishment of foreign aid and development efforts in the nations in need, it can also lead to vulnerabilities, specifically during periods of dollar appreciation, which may exacerbate existing economic conditions and hinder growth prospects.

Therefore, the interplay between the US dollar, global economic conditions, and emerging market dynamics represents a critical area of investigation, particularly in the context of evolving global economic governance structures. This paper delves into the historical underpinnings that have contributed to the dollar’s preeminent position, exploring its far-reaching consequences for various facets of the global economy. Additionally, it anticipates the prospective trajectories of both the dollar itself and other currencies within a perpetually shifting financial landscape.

In order to conduct a more in-depth and accurate analysis of the subject matter, the following definitions and concepts are provided: the World Bank – an international organisation dedicated to providing financing, advice, and research to developing nations to aid their economic advancement; the World Trade Organisation (WTO) – the only global international organisation dealing with the rules of trade between nations; the Gross Domestic Product (GDP) – a reference point for the health of national and global economies; the International Monetary Fund (IMF) – an international organisation that promotes global economic growth and financial stability, encourages international trade, and reduces poverty; monetary policy – a set of tools used by a nation’s central bank to control the overall money supply and promote economic growth and employ strategies such as revising interest rates and changing bank reserve requirements; the Gold Standard – a system under which countries fix the value of their currencies in terms of a specified amount of gold; a Financial Center – an area (it may be a city, county, or somewhere larger) where there is a high concentration of financial institutions; reserve currency – a large amount of currency held by central banks and major financial institutions to use for international transactions; the primary reserve currency – the most held reserve currency and the most widely used currency for international trade and other transactions around the world; the Society for Worldwide Interbank Financial Telecommunication (SWIFT) – a system that powers most international monetary and security transfers, a global messaging network used by financial institutions to quickly, accurately, and securely transmit and receive information, such as monetary transfers; Dow Jones (Dow Jones & Company) – one of the world’s largest business and financial news companies; DJIA – the Dow Jones Industrial Average; currency convertibility – the ease with which a country’s currency can be converted into gold or another currency; (sovereign) default – the failure by a country’s government to pay its debt; a recession – a significant, widespread, and prolonged downturn in economic activity; debt “sustainability” – the ability of a country to meet its debt obligations without requiring debt relief or accumulating arrear; austerity – characterises severity or sternness and describes economic measures implemented by a government to reduce public-sector debt by significantly curtailing government spending; inflation – the rate of increase in prices over a given period of time; de-dollarisation – a significant reduction in the use of dollars in world trade and financial transactions, decreasing national, institutional and corporate demand for the greenback; reserve assets – financial assets denominated in foreign currencies held by central banks and used to balance payments.

1.1 Literature Review

In this research project, we used and analysed such works and concepts as stated in ‘The Dollar Cycle of International Development’ published in the Springer journal (Hung & Liu, 2021), ‘The Rise and Fall of Global Currencies over Two Centuries’ published in the Social Science Research Network (SSRN), (Vicquéry, 2022) and ‘The Changing World Order’ which was authored by Ray Dalio (Dalio, 2021, 331-363).

The Springer article presents an institutional perspective, focusing on the role international institutions play in shaping global economic policies. It argues that institutions such as the IMF and World Bank are crucial in maintaining stability and facilitating dominance of the US dollar. Highlighting China’s rise, the article suggests that reforms are required to accommodate more economic powers and emerging economies, emphasising the need for institutional adaptability in reshaping global currency dominance. Meanwhile, the SSRN paper introduces a network theory approach, emphasising the interconnectedness of global financial systems. This perspective posits that currency dominance is influenced by network effects within global trade and finance, with the US dollar maintaining its position due to entrenched networks and widespread use in international trade. Ray Dalio’s book, however, offers a cyclical theory of global currency dominance based on the historical rise and decline of previous major economic powers. Dalio identifies key stages in the life cycle of these dominant currencies, arguing that economic, political, and social factors contribute to these cycles.

From the analysis of these works we have managed to merge the three schools of thought provided by the literature, as the following sections discuss the shift from the Pound Sterling to the US dollar, the role of the IMF and the World Bank in the dominance and mechanisms of the US dollar, and the implications of this dominance in the present and the future.

2. Historical Context

2.1 Rise of the British Pound

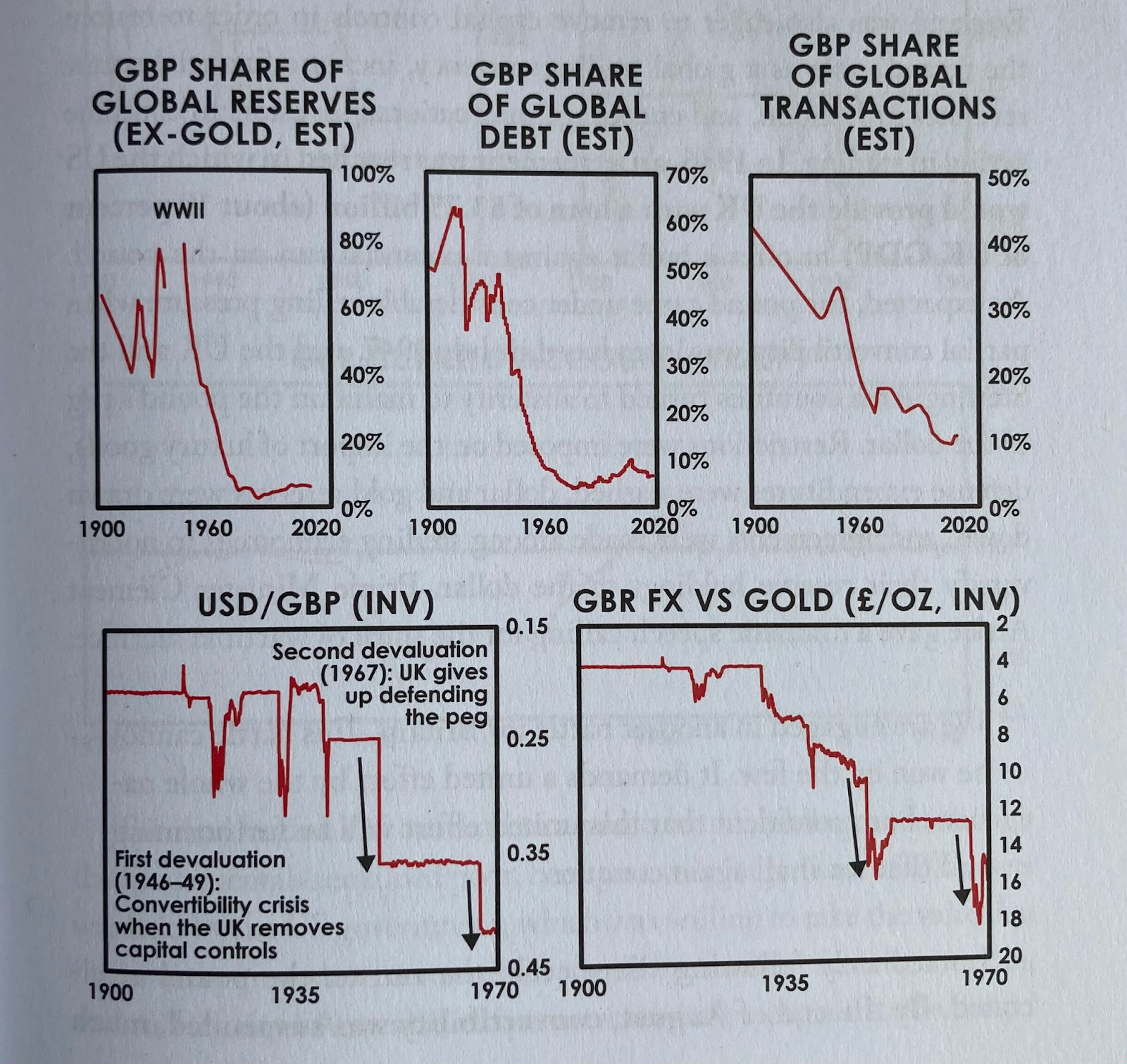

Following the establishment of the Bank of England in 1694, Britain gained a reliable banking system which successfully monitored the country’s monetary policy. Therefore, the pound sterling was viewed as a currency with a stable value, considering the Bank of England had the ability to exchange the bank notes for set amounts of gold which derived from various gold reserves in multiple of the British Empire’s colonies. Henceforth, in 1821, Britain was issued the gold standard which increased the pound’s strength in global trade. By then, the pound sterling was already utilised in over 60% of international trade exchanges, and it gradually began to dominate an even more significant percentage during the following years (Wikipedia, n.d.).

Additionally, the vastness of the British Empire meant that Britain owned an abundance of raw materials and primary resources from several of its colonies, which were prominent in international trade. Therefore, the use of the pound sterling also facilitated trade amongst the extensive network of colonies and the rest of the world. Moreover, London’s role as one of the leading financial centres worldwide in 1914 had led to increasing demand for the pound worldwide, following numerous investments which required foreign currency transactions. Consequently, the pound sterling became the primary reserve currency during the 19th century and early 20th century (Bo S. Karlstroem, 1967).

Aside from further enhancing Britain’s position in international trade, the rise of the pound sterling as a reserve currency resulted in various implications for the country. Firstly, its increasing strength and dominance encouraged Britain’s industrialisation, as their dominant position in world trade increased demand for manufactured goods. Britain’s successful shift to the secondary sector was reflected by the fact that it was the first country to enjoy the various benefits which stemmed from the Industrial Revolution. This not only further boosted British exports for manufactured goods, but also commenced a trend amongst other countries which encouraged country specific industrial revolutions, as they were inspired by the result of Britain’s successful increase in mechanisation. Moreover, it expedited financial exchanges amongst British colonies, which allowed for the growth of the Empire, as well as improving the efficiency of said transactions. Overall, the predominance of the pound sterling during the period in which it was the primary reserve currency aided in boosting Britain’s position in global trade, as well as preserving the currency’s stability.

2.2 The Bretton Woods Agreement

Nearing the end of the Second World War, post-war economic recovery was a pressing issue for most countries which had faced financial instability due to the consequences of the war. Therefore, there was a need for a foreign exchange system which aimed at promoting economic growth on an international level. While the system of the gold standard was successful at maintaining stability, it was considered too rigid. This was particularly negative during war as it restricted central banks from modifying their monetary policy according to the fluctuating state of the economy. On the contrary though, there was a strong need for a balancing system to prevent countries from devaluing their currency in order to boost trade by offering more competitive prices to the market. Therefore, in July 1944, a conference was held in Bretton woods which hosted 730 delegates from 44 countries, which aimed to agree on solutions for the issues surrounding currency exchange rates.

The system created was called the Bretton Woods system, which provided the necessary framework to make currency exchange rates fixed internationally. This was monitored by the IMF, which was created as a consequence of this agreement. It ensured that each country would abide by the set standard for each currency’s correspondence to the US dollar and required that each country upheld the said standard. Even though it was an individual responsibility of each individual member state to align the strength of their currency within the 1% fluctuating boundary set by the IMF, it would lend loans to those who underwent a significant economic crisis (Garber, n.d.).

Undoubtedly, the region most affected by World War II was Europe, so to aid Europe in undergoing economic recovery, the United States devised the Marshall Plan (1948). It is estimated that Europe faced about $1 trillion in economic damages due to the war. The United States gave approximately $13.3 billion to capitalistic Western European countries in order to accelerate their economic recovery (National Archives, 2022). Similarly, the United States gave Japan approximately $2.2 billion to aid (between 1946-1952) their economic recovery as part of the Dodge Plan. These generous deals asserted the United States as the dominant global economic power. After World War II, the United States dollar was all set to take over the British pound sterling.

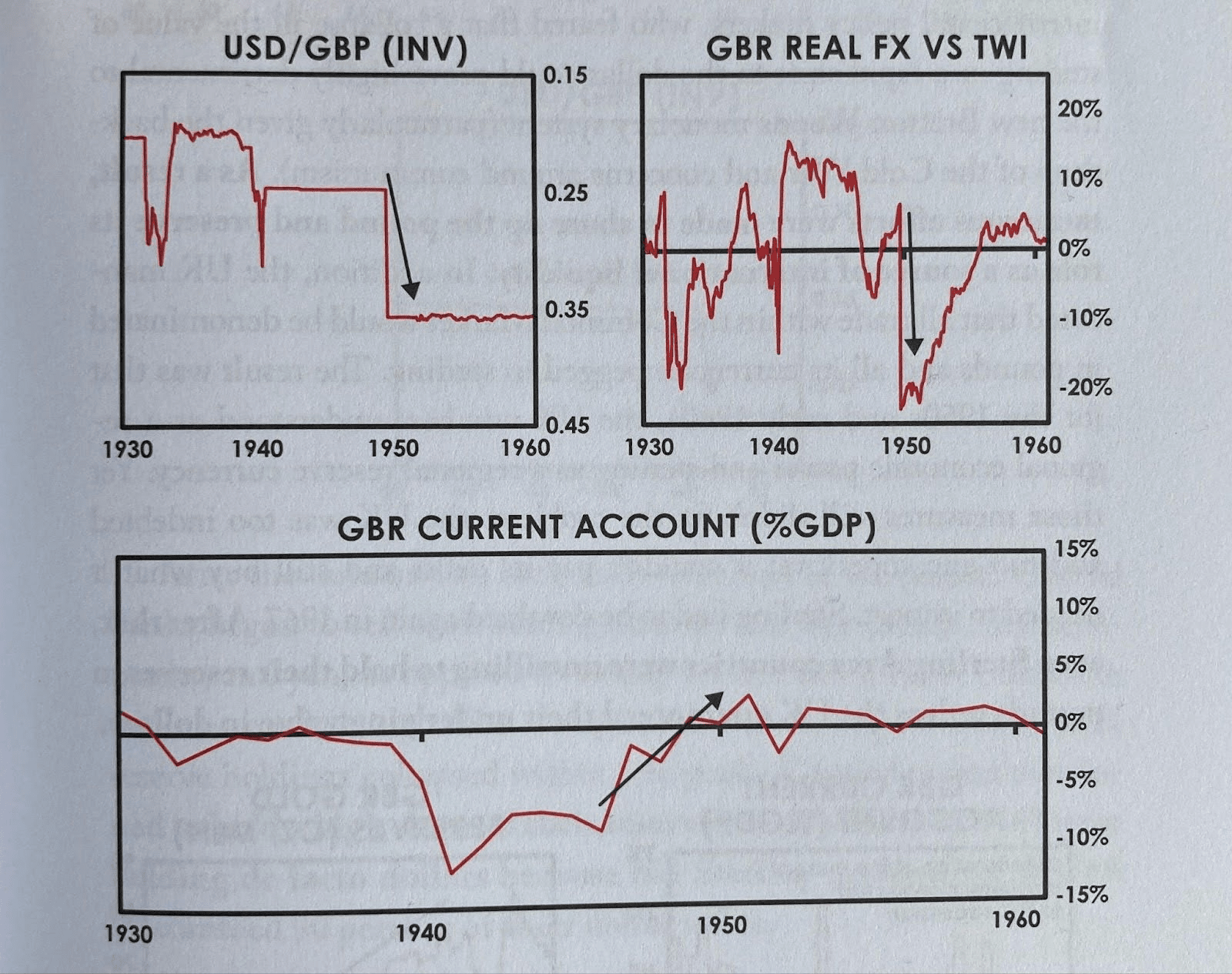

Convertibility was reintroduced for the British pound after World War II in July of 1947. Naturally, governments and investors all around the world traded huge amounts of the pound for the dollar. To keep the exchange rate at a high enough number, the United Kingdom suspended convertibility in August. This angered the United States and investors who had bought assets using pounds. Prior to restoring convertibility in 1950, the Bank of England resolved to devalue the pound to get closer to a fair exchange rate.

Throughout the 1950s and 60s, a lot of capital was used to keep the pound as the dominant global currency. However, the United Kingdom had begun to default on its international debts and could not compete with the United States. The pound was devalued yet again in 1967. Constant devaluations and financial instability in the United Kingdom led to countries around the world to reduce the proportion of pounds in their reserves.

At the same time, the United States was prospering. After a brief post-war recession (due to a decrease in military spending), the United States prospered as it became the most dominant industrial power.

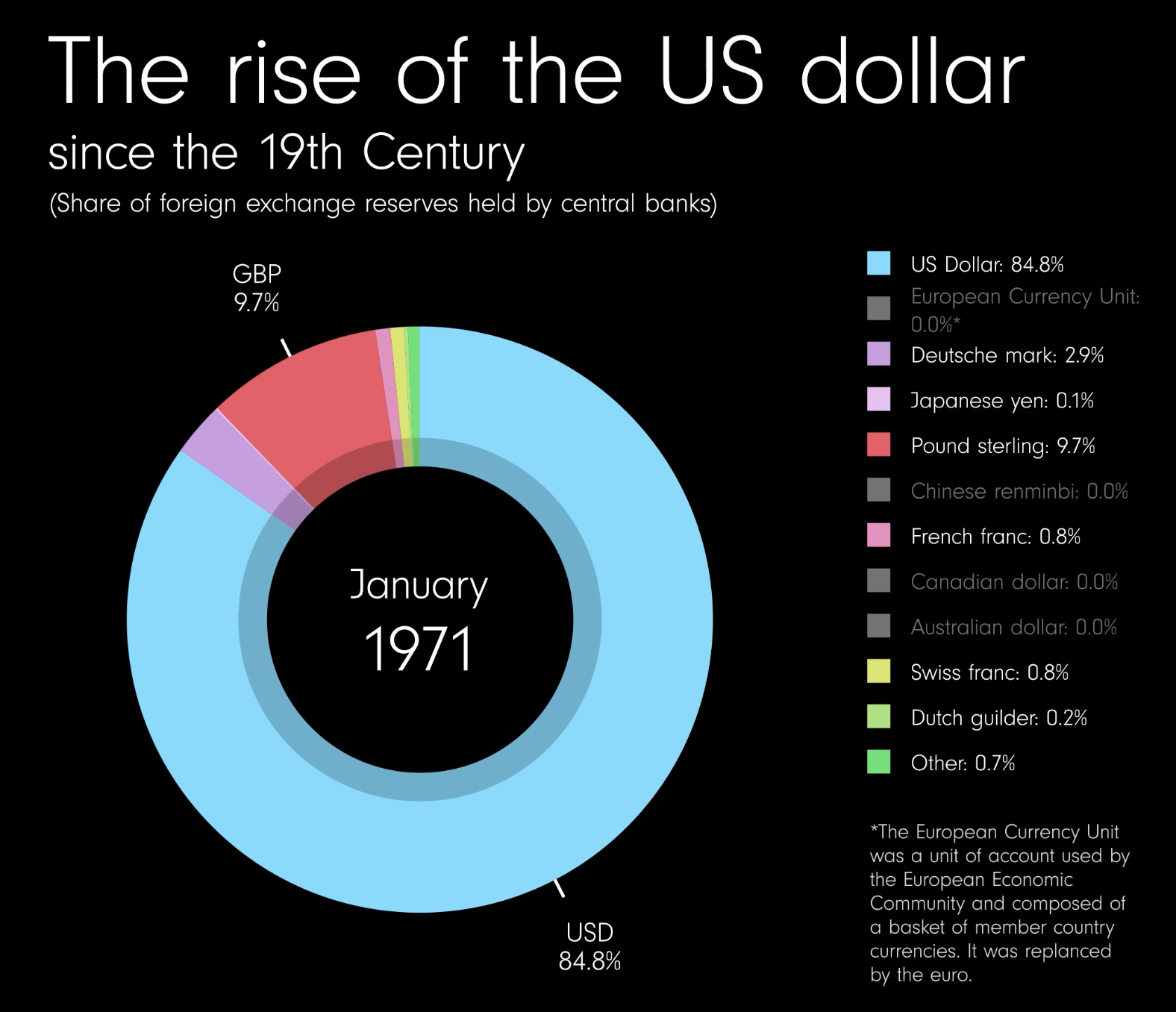

The Marshall and Dodge Plans, coupled with American economic prosperity, encouraged countries from around the world to hold more dollars and less pounds in their reserves throughout the late 20th century. The Dow Jones reached close to 10,000 points for the time in January 1966 when it hit 9,717.08 points (The Dow Jones Industrial Average, n.d.). By the end of 1970, about 85% of global reserve currency held was the USD (Eagle & Neufeld, 2023).

However, the United States faced a problem throughout the 1960s: rampant inflation. The payments deficit was increasing due to excessive spending on the Vietnam War, spending a total of $176 billion (The Digital History, n.d.). Whilst funding the military, the Federal Reserve did not leave enough money to cover their domestic deficit. The Federal Reserve also miscalculated the unemployment rate before drafting lavish spending policies. This led to sky-high inflation, which peaked at 6.2% in 1969. This situation is perfectly encapsulated by the words of McChesney Martin, the chair of the Federal Reserve from 1951 to 1970, who famously said: ‘We could not have guns and butter’ (Marsh, 2021).

At this point, the US owned a significant percentage of global gold reserves, so it was issued the gold standard. This system dominated throughout the 1970s, but as predicted by economist Triffin in 1960, the policy was proven to be very feeble for multiple reasons. Beginning from 1959, the supply of US dollars began to exponentially increase worldwide, while gold was becoming increasingly more scarce. This led to the overvaluation of the currency.

Therefore, on the first of November in 1961, eight central banks in the US, along with seven European countries combined their gold reserves to maintain the gold price of 35$ per ounce, which was set by the Bretton Woods system. This was called the London Gold Pool. It was successful for six years until its collapse in March 1968 as the pegged price of gold remained too low. During this period, a total of three billion dollars’ worth of gold was sold, which caused an 18% decline in gold stocks between September 1967 and March 1968. Consequently, President Richard Nixon suspended the Bretton Woods system on the 15th of August 1971 as this overvaluation threatened US trade. Attempts were made to continue the baseline of this system by devaluing the dollar (Humpage, n.d.).

The first attempt was made in December of 1971 and was named the Smithsonian Agreement. It was led by monetary authorities from ten of the world’s leading countries, where they agreed to devalue the dollar by 8.5% (38$/ounce). This meeting held in Washington DC was considered to be “the most significant monetary agreement in the history of the world” according to Nixon, but its longevity was challenged by pressure in global financial markets. During the following months, efforts were continuously made to sustain the Bretton Woods agreement, but as of March 1973, all efforts were abandoned (Garber, n.d.).

2.3 The Decline of the USD

Arguably, the decline of the dollar began after the Smithsonian Agreement. Since the collapse of the Soviet Union in 1991, the United States (and by extension the whole world) has been hit with three major financial crises: namely the 2000 dot-com bubble (and the recession that followed), the 2008 financial crisis and the 2020 coronavirus-induced economic downturn. Throughout these years (1991-present day), the United States has lost its position as the industrial capital of the world. In 2000, the United States’ balance of trade was approximately negative $436,000. On the other hand, China’s balance of trade was slightly positive at around $24,000 (World Integrated Trade Solution, n.d.). Today, the situation is overwhelmingly in China’s favour. The United States had a trade deficit of $773 billion in 2023, while China had a positive balance of trade at around $823 billion (Statista Research Department, 2024). This has led to American goods losing competitiveness in global markets to cheaper and more abundant Chinese goods.

To guide themselves through the three major financial crises of the 21st century, the United States primarily used “debt-financed spending”. Interest rates fell to 0% during crises and huge sums of money were printed by the Federal Reserve. American national debt has ballooned from around $8.5 trillion in 2006 to $35 trillion currently. Although the United States has a lower debt-to-GDP-ratio than China, such fiscal policies undermine the dollar’s status as a stable currency. A prime example of the United States not being able to manage their debt is the 2023 debt-ceiling crisis, when the American debt ceiling of $31.4 trillion was breached. President Biden suspended the debt ceiling completely until January 1, 2025 by passing the Fiscal Responsibility Act. Such a recent crisis shows us that the United States is quite vulnerable to defaulting on its debts.

Another factor to consider while looking at the position of the dollar as the dominant global currency is the political stability in the United States. Under the Trump administration, income and wealth gaps diverged significantly. President Trump’s radical conservative pro-business policies has led to political polarisation amongst the American parties and people as a whole. A country undergoing economic decline is often characterised by escalating internal conflict, which we are certainly observing in the United States.

3. The US Dollar’s Dominance

3.1 Trade Cycle: World Trade Organization

In today’s interconnected economy, the US dollar has a unique significance. The dollar entered the global market and became the dominant global reserve currency after World War I, when countries pegged their currencies to it to facilitate international trade. For most of the past century, this prominent position has been supported by the strength and size of America’s economy, as well as its stability and openness to international trade and capital movements. The US dollar in international trade is seen as a safe haven currency, meaning that investors often flock to it during times of economic uncertainty. Finally, the US government and central bank, the Federal Reserve, have a strong track record of maintaining the dollar’s stability, which has helped to build trust in the currency and further cement its position as the dominant currency in international markets. This has also been facilitated by the rule of law and the protection of property rights in the country. Due to these factors, the dollar has emerged as the dominant currency for international transactions, and its use in financial markets is widespread. This is because its large economy, with a gross domestic product (GDP) larger than the combined GDPs of the next three largest economies, makes it a convenient choice for conducting international business. Nevertheless, the ease of converting the dollar into other currencies further enhances its attractiveness for global transactions.

Overall, the dominance of the US dollar in international transactions and financial markets can be attributed to a combination of several factors. These factors include the size and strength of the US economy, the stability of its political system, the sophistication of its financial institutions, its long history of international trade and investment, and its military and diplomatic influence. These factors, when taken together, have contributed to the position of the dollar as the dominant global reserve currency (World Trade Organization, 2023). In global trade, the exchange rate of the US dollar is an important factor that is closely linked to conditions in the international financial market. This tends to fluctuate cyclically, and when the dollar strengthens, it can signal an economic slowdown in emerging markets. The appreciation of the dollar can be associated with several factors, including the tightening of monetary policy in the United States and indicators of financial stress and risks for investors in the dollar. This could present challenges for emerging market economies, as they may face higher interest rates and slower economic growth as a result of increased debt incurred during the crisis and the impact of a stronger dollar (Obstfeld & Zhou, 2022, 361-447).

3.2 Developing Economies and the Role of the World Bank and the IMF

The World Bank and the IMF are pivotal institutions in the global economic landscape, particularly concerning the development and financial stability of emerging economies. Both organisations provide crucial financial assistance and policy guidance to developing countries, albeit with distinct mandates and operational focuses. This section critically examines the roles of the World Bank and IMF in fostering economic development, the mechanisms through which they operate, and the implications of their interventions on developing economies.

a) The Mandates and Functions of the World Bank and IMF

The World Bank and the IMF were established at the Bretton Woods Conference in 1944 to promote international economic cooperation and stability. Despite their shared origins, the two institutions have distinct mandates. The World Bank’s primary objective is long-term economic development and poverty reduction, whereas the IMF focuses on ensuring global macroeconomic and financial stability (International Monetary Fund, n.d.).

The World Bank Group comprises five institutions, which provide financial and technical assistance to middle-income and creditworthy low-income countries. The World Bank’s financial assistance encompasses low-interest loans, zero to low-interest credits, and grants. These resources are directed towards various developmental projects, such as infrastructure, education, health, and agriculture, aimed at fostering sustainable economic growth and improving living standards. Additionally, the World Bank offers extensive technical assistance, which includes research, analysis, policy advice, and capacity-building support to help countries implement effective development strategies (World Bank, n.d.).

The IMF primarily provides short- and medium-term financial assistance to countries facing balance of payments problems. This assistance aims to stabilise economies by supporting exchange rate stability, preventing competitive devaluations, and perpetuating global monetary cooperation. The IMF’s financial support often comes with conditions that require the recipient country to implement specific economic policies, known as conditionality, to address underlying structural weaknesses and restore economic stability. In addition to financial assistance, the IMF offers policy advice and capacity development support. The IMF monitors the global economy and provides recommendations to member countries on macroeconomic policies, financial sector reforms, and structural adjustments (International Monetary Fund, n.d.).

b) The Role of the US Dollar in World Bank and IMF Operations

The US dollar’s dominance in the global economy influences the operations of both the World Bank and the IMF. As the primary reserve currency, the US dollar serves as the standard denomination for international loans, financial assistance, and debt repayment mechanisms provided by these institutions. The World Bank and IMF predominantly extend their financial assistance in US dollars. This practice underscores the dollar’s centrality in global finance, but also exposes developing countries to significant risks associated with exchange rate fluctuations and dollar appreciation. For instance, when the US dollar strengthens, the debt servicing costs for dollar-denominated loans increase, straining the financial resources of developing economies. Dollar-denominated debt creates a dependency on the US dollar, compelling developing countries to maintain substantial dollar reserves to manage their international obligations. This dependency can lead to vulnerabilities in the face of global financial shocks, as witnessed during the COVID-19 pandemic when sudden capital outflows and currency depreciations exacerbated the financial instability of many emerging markets.

Countries receiving dollar-denominated loans are exposed to exchange rate risks. Any depreciation of the local currency against the US dollar increases the burden of debt repayment, potentially leading to balance of payments crises and necessitating further financial assistance. Developing countries with significant dollar-denominated debt may face constraints in their monetary policy. To maintain currency stability and manage debt obligations, these countries often need to implement tighter monetary policies, which can stifle economic growth and investment (Ocampo, 2017). The need to accumulate and maintain large dollar reserves can lead to inflationary pressures in developing economies. Excessive dollar accumulation may require expansive monetary policies, increasing domestic money supply and potentially leading to inflation.

c) Mechanisms of Assistance and Conditionality

Both the World Bank and the IMF employ a variety of mechanisms to deliver assistance to developing countries. However, the conditions attached to their support have significant implications for the recipient countries’ economic policies and governance. The World Bank’s financial instruments include investment loans, development policy loans, and programme-for-results loans. Investment loans finance specific projects, such as infrastructure development or social programmes, while development policy loans provide budget support to help countries implement policy reforms. Programme-for-results loans link disbursements to the achievement of specific outcomes, thereby enhancing accountability and ensuring that funds are used effectively. Technical assistance from the World Bank includes a wide range of services, such as economic research, policy analysis, and capacity-building initiatives. These services aim to enhance the recipient countries’ ability to design and implement effective development policies, thereby promoting sustainable economic growth and reducing poverty (World Bank, n.d.).

The IMF’s primary financial instruments include Stand-By Arrangements (SBAs), Extended Fund Facility (EFF), and Rapid Financing Instrument (RFI). SBAs provide short-term financial support to address balance of payments needs, while the EFF offers medium-term assistance for structural reforms. The RFI provides rapid financial assistance with limited conditionality to countries facing urgent balance of payments needs due to external shocks (International Monetary Fund, n.d.).

Conditionality is a cornerstone of IMF assistance, requiring recipient countries to implement specific economic policies to address underlying structural issues. These conditions often include fiscal austerity measures, such as reducing budget deficits and public debt, implementing tax reforms, and cutting public expenditure. While these measures aim to restore macroeconomic stability, they can also lead to short-term economic hardship and social unrest. Critics argue that IMF conditionality can be excessively stringent, prioritising financial stability over social and economic development. For example, austerity measures can exacerbate poverty and inequality by reducing public spending on essential services, such as healthcare and education. Additionally, structural adjustment programmes (SAPs) have been criticised for promoting neoliberal economic policies that may not align with the developmental needs and socio-political contexts of recipient countries. The World Bank also employs conditionality, albeit with a focus on long-term development outcomes. Conditionality in World Bank loans often involves policy reforms aimed at improving governance, enhancing institutional capacity, and promoting sustainable development. However, like the IMF, the World Bank’s conditionality has faced criticism for promoting policy prescriptions that may not be suitable for all countries (Easterly, 2000).

d) Implications for Developing Economies

The financial assistance and policy advice from the World Bank and IMF significantly impact the economic policies and governance of developing countries. Conditions attached to their support often require major policy changes, which can limit policy autonomy and hinder long-term development. For instance, IMF-imposed austerity measures can restrict investment in social programmes and infrastructure (Ocampo, 2017). While World Bank and IMF assistance has improved infrastructure, education, and healthcare, it can also lead to negative social impacts like increased poverty and inequality. Austerity measures have been linked to reduced public spending and worsened health and education outcomes (Kentikelenis et al., 2016). Structural adjustment programmes can cause economic disruptions and job losses, increasing poverty and social unrest. Dollar-denominated debt, a common feature of World Bank and IMF loans, exposes developing countries to exchange rate risks and financial instability, as they cannot print dollars to repay debts. High external debt can lead to debt crises, affecting financial stability and economic growth. Despite efforts to ensure debt sustainability through fiscal austerity and structural reforms, these measures can constrain economic growth and development.

e) The Role of the US Dollar in Development Finance

Developing countries often face currency mismatches, where their liabilities are denominated in foreign currencies (primarily the US dollar), while their assets and revenues are in local currencies. This mismatch exacerbates financial vulnerabilities, as depreciation of the local currency increases the burden of dollar-denominated debt, potentially leading to liquidity crises and defaults. The predominance of the US dollar also affects trade and investment flows. Dollar depreciation can make exports from developing countries more expensive and less competitive, reducing their trade balances and economic growth. Conversely, a strong dollar can attract capital inflows to developing countries seeking higher returns, but these inflows can be volatile and subject to sudden reversals, exacerbating financial instability (Ocampo, 2017).

3.3 Financial Stability: IMF

The US dollar continues to be the dominant reserve currency. However, it is losing its position to other non-traditional currencies (Australian dollar, Canadian dollar, Chinese yuan, South Korean won, Singapore dollar, and Scandinavian currencies). Several factors have contributed to this shift, including the resilience of the US economy, the implementation of tighter monetary policies, and the increasing geopolitical risks.

The IMF has observed a decline in the proportion of US dollars in allocated foreign reserves maintained by central banks and government entities over time. This trend indicates a move towards diversifying the currency composition of reserve assets. Notwithstanding these factors, there has been a gradual shift away from the dominance of the US dollar in the composition of global foreign exchange reserves.

The growing popularity of alternative currencies reflects central bankers’ desire to diversify investment portfolios and achieve higher returns. With the advent of digital financial technologies, buying, selling, and holding these currencies has become easier. These developments occur against the backdrop of increasing dollar dominance. It is important to note that exchange rate fluctuations and changes in government securities’ relative values can independently influence central bank reserve currency composition. Over the last two decades, the dollar’s share in world reserves has decreased, indicating a shift away from central banks’ reliance on the dollar.

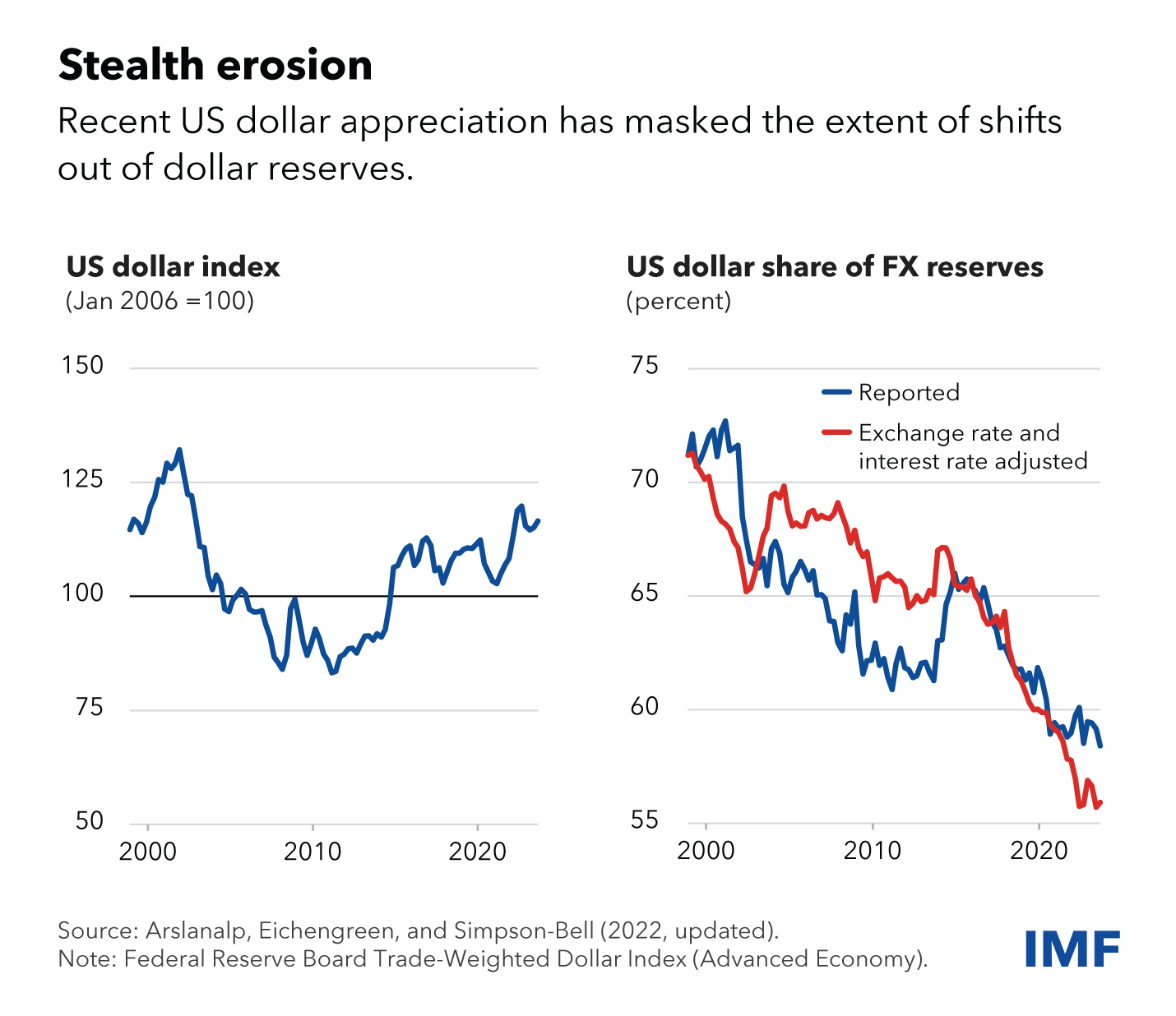

The chart of trends above corroborates the aforementioned information and demonstrates that investors are shifting their investments towards dollar-denominated assets, while central banks are progressively diminishing their reliance on the US dollar (Arslanalp et al., 2024). It is also important to mention the gold collateral of the dollar. The US had the opportunity to continue to create a debt-backed currency, which led to a decrease in the value of the dollar’s gold collateral. This increase in the money supply in relation to gold and foreign exchange reserves led to a decrease in the foreign exchange reserves of other countries, which caused concern in some countries, which became another reason for “distrust” of the dollar (Lioudis et al., 2024). However, what is the relevance of the correlation between the dollar and gold? As it relates to linking the foreign exchange rate of a nation’s currency with the dollar, there emerged the notion of establishing the dollar as the sole currency backed by gold. To address this issue, two new international financial entities were established: the IMF and the International Bank for Reconstruction and Development (IBRD).

It is important to consider the relationship between the US dollar and gold in today’s global monetary system. For a significant period of time, gold served as the primary reserve currency, but after the abandonment of the gold standard, its value declined. However, in recent years, there has been a renewed interest in using gold as collateral, particularly following the Great Recession, thanks to new capital requirements and the increased liquidity of the market for gold as an asset. The well-established liquidity of the global gold market across various time zones continues to contribute to its significance in the financial system. Gold continues to play an important role in the global financial system, serving as both a medium of exchange and a collateral asset. As investors purchase gold, its value increases, while the value of the US dollar decreases. This raises the question of what factors influence the correlation between gold and the US dollar. In the past, gold served as the primary medium of exchange before World War I. Subsequently, it was replaced by paper currency, and central banks began discussing the need for a more stable financial system to facilitate trade. Before the adoption of the gold standard, which involved the use of gold in US dollar transactions, countries experienced fluctuations in exchange rates during World War II. These fluctuations resulted from differences in exchange rates among countries, which were caused by variations in the way countries set monetary values for transactions. Some countries utilised weak currencies to benefit from export activities, whereas others relied on gold reserves to maintain exchange rate stability. This situation led to a stagnation in international investment and trade as well as disputes between nations. Many nations imposed trade restrictions through the implementation of high taxes and subsidies for exports in order to protect their domestic economies. These policies created obstacles to trade and investment, resulting in conflicts and the onset of World War II. Gold has long been associated with the US dollar and its value has been tied to that of the latter. This arrangement has helped maintain stability in international trade and financial transactions, but it has also posed challenges for countries seeking to diversify their economic bases and reduce their reliance on the dollar. Fluctuations in the value of the US dollar may impact the price of gold. When the dollar’s value declines relative to major world currencies such as the Euro and Japanese Yen, the price of gold tends to rise. This occurs because the price of gold is expressed in US dollars, and as the dollar’s worth diminishes, gold becomes comparatively less expensive compared to other currencies held by investors. Consequently, this leads to an increased demand for gold, resulting in a rise in its price. The relationship between gold and the US dollar dates back to the early 20th century and has continued to evolve as the global financial landscape has developed. While the US dollar plays a significant role in determining gold prices, other factors such as monetary policy, supply and demand, oil prices, and global economic conditions also influence the gold market. Investors who understand these factors and adopt a well-informed gold investment strategy may benefit from long-term returns (Siam Commercial Bank, n.d.).

4. Implications of the Dominance: Sanctions Following the Russo-Ukraine War

The dominance of the US dollar in the global financial system endows the United States with substantial geopolitical leverage, particularly through the imposition of economic sanctions. The Russo-Ukraine war has shed some light on the extent of this power, following the numerous sanctions imposed upon Russia by the United States since the invasion of Ukraine. This section delves into the mechanisms of sanctions, their implications for the global financial system, and the broader consequences for international currency systems.

4.1 Mechanisms of Sanctions and the US Dollar’s Role

Sanctions are defined as punitive measures or actions that are imposed on a country to compel it into complying with the international rules and regulations set. The US dollar’s dominance enhances the efficiency of these sanctions, given its central role in global trade and finance. By leveraging the dollar-dominated financial system, the United States has imposed severe restrictions on countries like Russia, substantially disrupting their economic operations. As most international trade transactions are conducted with the US dollar being the primary currency, the United States can exert significant pressure on Russia by restricting its access to the supply of the dollar, as well as their inherent access to the dollar-based financial system.

The US-imposed sanctions on the Russian financial sector include the freezing of $5 billion of the Russian central bank’s US dollar assets to prevent the nation from using the global currency as its foreign reserve to support the Russian Ruble (Maizland & Berman, 2024). Moreover, approximately $350 billion of Russia’s foreign currency reserves, representing half of its total reserves, have been frozen (British Broadcasting Corporation, 2024). As previously mentioned, major Russian banks were barred and removed from the Society for Worldwide Interbank Financial Telecommunications (SWIFT) system, which is responsible for most international money and security transfers (Seth, 2023). Additionally, the United States has commenced with a total ban on the import of Russian crude oil and coal as of March 2022, further encouraging other prominent nations in the global economy such as the European Union to prohibit seaborne crude imports from Russia. The United States, alongside its Group of Seven (G7) allies, have implemented price caps on Russian crude oil to limit the revenue Russia could generate from its energy exports. The US Commerce Department has further restricted exports of high-tech products, including aircraft equipment and semiconductors, to curtail Russia’s military capabilities. Moreover, several Western nations have prohibited the export of technology that could aid in weapon production. The US has leveraged the dollar’s status as the world’s leading reserve currency to freeze foreign actors’ dollar-based assets, effectively cutting adversaries off from their financial wealth. In response to sanctions, Russia has pursued de-dollarisation policies to reduce its dependence on the US dollar and mitigate political risks. This includes diversifying its foreign reserves and promoting the use of alternative currencies. Sanctions have led to a contraction in Russia’s economy, with a 2.1% decline in 2022, although a slight growth of 2.2% was recorded in 2023. The US Treasury estimates that sanctions have hindered Russia’s economic expansion by 5% over the past two years (British Broadcasting Corporation, 2024).

4.2 Impact on the Global Financial System

The imposition of extensive sanctions has had a multitude of implications for the global financial system. One notable effect has been a reduction in the dollar’s share of global reserve currencies. Despite its continued dominance, the extensive use of sanctions has prompted countries to reconsider their reliance on the dollar and explore alternative financial systems. Sanctions against Russia have exposed vulnerabilities in the financial systems of countries heavily reliant on dollar-denominated transactions. For instance, the freezing of Russian reserves and restrictions on dollar-based financial transactions have disrupted Russia’s economic activities and international trade. This disruption has driven some countries to seek alternatives to mitigate the risks associated with reliance on the dollar. In addition, the sanctions have intensified the scrutiny of the global financial system’s dependence on a single dominant currency. This overreliance on the dollar makes the global economy susceptible to geopolitical conflicts and unilateral actions by the United States. As a result, there is a growing discourse on the need for a more diversified global financial system to enhance stability and reduce vulnerabilities.

4.3 Emergence of De-Dollarisation Efforts

The sanctions imposed on Russia have accelerated efforts toward de-dollarisation, as countries seek to mitigate the risks associated with dollar dependence. De-dollarisation involves reducing reliance on the US dollar for international transactions and reserves, thereby diminishing the economic leverage of the United States.

A key example of de-dollarisation is Russia’s increased use of the Chinese yuan in international transactions. In response to sanctions, Russia has expanded its financial and trade interactions with China, utilising the yuan as a substitute for the dollar (den Besten et al., n.d.). This shift reflects a strategic move to mitigate the impact of US financial sanctions and enhance financial autonomy. Moreover, the sanctions have spurred interest in alternative reserve assets such as gold. Countries aligned with China and Russia have increased their gold holdings to hedge against the risks posed by dollar dominance. As of July 2022, Russia’s gold reserves stood at 2,298.53 tons (Wenhong, 2023, 9-18). More than 90% of mutual payments between Russia and China are now made in rubles or yuan, indicating a significant shift away from the US dollar in bilateral trade. This shift is part of a broader trend of de-dollarisation in their economic relations (Ramos & Rocha, 2024). This trend underscores a broader effort to diversify reserves and seek refuge in non-traditional reserve assets.

4.4 Long-Term Implications for the Dollar’s Dominance

While the US dollar remains dominant in global finance, the long-term implications of sanctions and de-dollarisation efforts are far-reaching. The extensive use of sanctions has the potential to gradually erode the dollar’s preeminence, as countries seek alternatives to mitigate geopolitical risks and enhance financial sovereignty. In the short term, the dollar’s dominance remains robust, with over 80% of global trade finance conducted in dollars. However, the growing trend towards de-dollarisation and diversification of reserve assets could reshape the global financial landscape over time. The network effects and economic incentives that currently support the dollar’s dominance are significant, but they are not immune to long-term shifts driven by geopolitical and economic factors. The potential emergence of a multipolar currency system, characterised by increased use of alternative currencies and reserve assets, could dilute the dollar’s dominance. This shift may alter the dynamics of global economic power and influence, leading to a more diversified and potentially less stable global financial system. Furthermore, the long-term impact of sanctions on the US dollar’s dominance will depend on several factors, including the effectiveness of alternative currencies in challenging the dollar’s role and the ability of the global financial system to adapt to evolving geopolitical and economic conditions. As countries continue to seek alternatives and diversify their reserves, the dollar’s role as the primary global currency may face significant challenges in the coming decades.

5. Implications for the Future

There is common consensus amongst economists that the dollar (and by extension the overall economic power of the United States) is on the decline. Two preeminent currencies stand out as the most likely successors of the dollar: the Chinese yuan (CNY) and the Indian rupee (INR).

One of the major factors affecting the economic position of a country is technological advancement and innovation. The World Intellectual Property Organization (WIPO), headquartered in Geneva, publishes a report each year about where each country stands based on technological innovation. Currently, the United States ranked third and China ranks twelfth in WIPO’s innovation rankings. Thus, the United States is the global leader in technological innovation.

However, the United States’ progress has been stagnant for over a decade now while China is improving each year. The United States was in third place in 2019 as well, while China was in 14th. China’s rapid rise can be put into perspective by the number of patents filed in each country. 501,513 patent applications were submitted in the United States (second in total patent applications) in 2013 and 515,281 in 2022, which is only an increase of ~2.5%. On the other hand, 734,115 applications were submitted in China (first in total patent applications) in 2013 and 1,586,339 in 2022, which is an increase of ~116%! India, despite ranking 40th in the WIPO innovation index, has outperformed China in terms of technological growth. 20,945 patent applications were submitted in India (seventh in total patent applications) in 2013 and 56,396 in 2022, which is an increase of ~169%.

Another factor to consider is population growth. To facilitate industrial and scientific growth, an abundant supply of labour (unskilled and skilled) is required. China has a fertility rate of 1.16, which is the lowest out of the three countries in question. The United States has a fertility rate of 1.66 and India has a fertility rate of 2.03. Of course, India’s fertility rate is the most optimal, showing that there is still a lot of industrial, economic, and scientific potential in India that can be utilised over the next 100 years. The same cannot be said for China (which is losing population) and the United States (whose population growth rate is a mere 0.4% and susceptible to decline due to a fertility well below the replacement level of 2.1), which relies almost exclusively on immigration to keep its population growing.

Due to stagnant or declining progress in the United States, the yuan and Indian rupee have a strong chance to take over as the global reserve currency.

6. Conclusion

This paper consolidates and ideates the implications of currency dominance, with special attention to the US dollar with regards to the role of supranational organisations and geopolitical leverages such as sanctions. Not only do fluctuations in the dollar affect monetary policies of multiple countries, but they also set global financial conditions. However, the process of de-dollarisation has commenced, and has imminent impacts on the emergence of new dominant currencies such as the Chinese yuan and the Indian rupee.

Bibliography

Arslanalp, S., Eichengreen, B., & Simpson-Bell, C. (2024, June 11). Dollar Dominance in the International Reserve System: An Update. International Monetary Fund (IMF). Retrieved July 27, 2024, from https://www.imf.org/en/Blogs/Articles/2024/06/11/dollar-dominance-in-the-international-reserve-system-an-update

British Broadcasting Corporation. (2024, February 23). What are the sanctions on Russia and have they affected its economy? BBC. Retrieved July 27, 2024, from https://www.bbc.com/news/world-europe-60125659

Dalio, R. (2021). Principles for Dealing with the Changing World Order: Why Nations Succeed and Fail. Simon & Schuster.

The Digital History. (n.d.). The War’s Costs. Digital History. Retrieved July 27, 2024, from https://www.digitalhistory.uh.edu/disp_textbook.cfm?smtid=2&psid=3468

The Dow Jones Industrial Average. (n.d.). Dow Jones – DJIA – 100 Year Historical Chart | MacroTrends. Macrotrends. Retrieved July 27, 2024, from https://www.macrotrends.net/1319/dow-jones-100-year-historical-chart

Eagle, J., & Neufeld, D. (2023, December 4). Visualizing the Rise of the U.S. Dollar Since the 19th Century. Visual Capitalist. Retrieved July 27, 2024, from https://www.visualcapitalist.com/cp/the-rise-of-us-dollar-since-19th-century/

Easterly, W. (2000, December). The Effect of IMF and World Bank Programs on Poverty. Social Science Research Network, 4. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=256883

Garber, P. M. (n.d.). The Collapse of the Bretton Woods Fixed Exchange Rate System. National Bureau of Economic Research. Retrieved July 24, 2024, from https://www.nber.org/system/files/chapters/c6876/c6876.pdf

Hughes, T. A., & Royde-Smith, J. G. (2024, July 27). World War II – Human Cost, Material Losses. Britannica. Retrieved July 27, 2024, from https://www.britannica.com/event/World-War-II/Human-and-material-cost

Humpage, O. (n.d.). The Smithsonian Agreement. Federal Reserve History. Retrieved July 24, 2024, from https://www.federalreservehistory.org/essays/smithsonian-agreement

Hung, H., & Liu, M. (2021, December 9). The Dollar Cycle of International Development. Studies in Comparative International Development, 35(1). https://doi.org/10.1007/s12116-021-09348-3

Kentikelenis, A. E., Stubbs, T. H., & King, L. P. (2016, May 24). IMF conditionality and development policy space, 1985–2014. Review of International Political Economy, 23(4), 543-582. https://www.tandfonline.com/doi/full/10.1080/09692290.2016.1174953

Lioudis, N., Boyle, M. J., & Reeves, M. (2024, June 10). What Is the Gold Standard? Advantages, Alternatives, and History. Investopedia. Retrieved July 27, 2024, from https://www.investopedia.com/ask/answers/09/gold-standard.asp

Maizland, L., & Berman, N. (2024, February 23). Two Years of War in Ukraine: Are Sanctions Against Russia Making a Difference? Council on Foreign Relations. Retrieved July 27, 2024, from https://www.cfr.org/in-brief/two-years-war-ukraine-are-sanctions-against-russia-making-difference

Marsh, D. (2021, November 22). Look at 1960s, not 1970s, to learn how US inflation took hold. OMFIF. Retrieved July 27, 2024, from https://www.omfif.org/2021/11/look-at-1960s-not-1970s-to-learn-how-us-inflation-took-hold/

Milestones in the History of U.S. Foreign Relations – Office of the Historian. (n.d.). Milestones in the History of U.S. Foreign Relations – Office of the Historian. Retrieved July 24, 2024, from https://history.state.gov/milestones/1969-1976/nixon-shock

National Archives. (2022, June 29). Home > Marshall Plan (1948). National Archives. Retrieved July 27, 2024, from https://www.archives.gov/milestone-documents/marshall-plan

Obstfeld, M., & Zhou, H. (2022). The Global Dollar Cycle. NATIONAL BUREAU OF ECONOMIC RESEARCH, 361-447. https://www.nber.org/papers/w31004

Ocampo, J. A. (2017). Resetting the International Monetary (Non)System. Oxford University Press.

Office of the Historian. (n.d.). Milestones in the History of U.S. Foreign Relations – Office of the Historian. Milestones in the History of U.S. Foreign Relations – Office of the Historian. Retrieved July 27, 2024, from https://history.state.gov/milestones/1969-1976/foreword

Ramos, M., & Rocha, A. P. (2024, May 29). Global South considers increasing de-dollarization, but Trump wants to punish those who reduce dependence on US currency. Brasil de Fato. Retrieved July 27, 2024, from https://www.brasildefato.com.br/2024/05/29/global-south-considers-increasing-de-dollarization-but-trump-wants-to-punish-those-who-reduce-dependence-on-us-currency

Seth, S. (2023, September 14). What Is the SWIFT Banking System? Investopedia. Retrieved July 27, 2024, from https://www.investopedia.com/articles/personal-finance/050515/how-swift-system-works.asp

Siam Commercial Bank. (n.d.). The relationship between gold and the dollar. SCB. Retrieved July 27, 2024, from https://www.scb.co.th/en/personal-banking/stories/grow-your-wealth/gold-and-dollar.html

Statista Research Department. (2024, July 5). Trade balance U.S. 2023. Statista. Retrieved July 27, 2024, from https://www.statista.com/statistics/220041/total-value-of-us-trade-balance-since-2000/

Vicquéry, R. (2022, July 21). The Rise and Fall of Global Currencies over Two Centuries. Social Science Research Network. https://papers.ssrn.com/sol3/papers.cfm?abstract_id=4205564

Wenhong, X. (2023). Dedollarization as a Direction of Russia’s Financial Policy in Current Conditions. Studies on Russian economic development, 34(1), 9-18. cbi.nlm.nih.gov/pmc/articles/PMC10072797/

World Integrated Trade Solution. (n.d.). United States Trade Summary 2000 | WITS | Text. World Integrated Trade Solution (WITS). Retrieved July 27, 2024, from https://wits.worldbank.org/CountryProfile/en/Country/USA/Year/2000/Summarytext

World Trade Organization. (2023, August 2). TTWTO VCCI – World Trade Statistical Review 2023. WTO Center. Retrieved July 27, 2024, from https://wtocenter.vn/an-pham/22462-world-trade-statistical-review-2023

{kind=link}